Key Takeaways

- If your 2026 Part B premium exceeds 2.90/month, IRMAA is the sole cause.

- Check your Medicare Initial Determination Notice from fall 2025 to identify your IRMAA tier and income year.

- Call Social Security at 1-800-772-1213 to confirm your current premium and the income year used.

- IRMAA surcharges are reversible, not permanent fixed costs, making proactive planning worthwhile.

- IRMAA affects both Original Medicare and Medicare Advantage enrollees equally.

Many households pay IRMAA surcharges for months before anyone explains why their Medicare bill is higher than the standard rate. This article helps you determine whether IRMAA is in your bill, what likely caused it, and what your actual options are now that you know.

IRMAA is not a fixed cost and it is not irreversible. The diagnosis and the response depend on where you are in the picture. Whether you are already on Medicare and trying to understand a higher-than-expected premium, approaching retirement, or managing RMDs year to year, this article addresses all three situations. This article addresses all three.

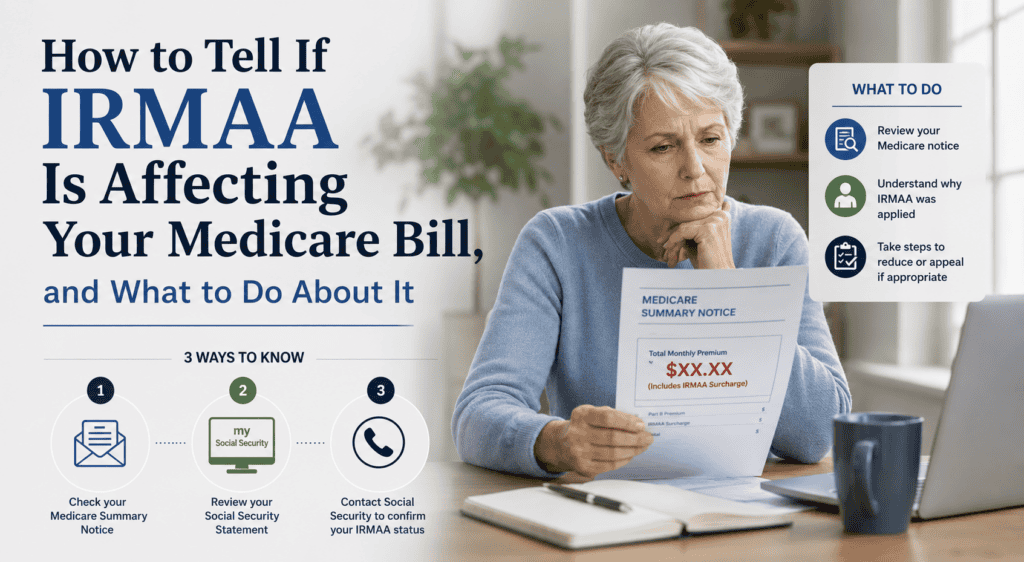

How to Tell If IRMAA Is in Your Medicare Bill Right Now

The first signal is your Medicare premium itself. The standard 2026 Part B premium is $202.90 per person per month. If the amount being deducted from your Social Security check, or billed directly, is higher than that, IRMAA is the reason. There is no other mechanism that raises the standard Part B premium above that amount.

If you are not yet sure what you are paying, check your Medicare Initial Determination Notice. This is the letter Social Security sent in the fall of 2025 before your 2026 premiums began. That letter states your Part B premium and, if applicable, identifies the IRMAA tier and the income year Medicare used to calculate it. If you did not receive this letter or cannot locate it, call Social Security at 1-800-772-1213 and ask for your current Part B premium amount and the income year used to set it.

IRMAA applies the same way regardless of whether you are enrolled in Original Medicare or a Medicare Advantage plan with drug coverage. The Part D surcharge also applies on top of whatever your individual drug plan charges, and it is paid separately to Medicare rather than to the insurer.

Confirm your number in two minutes

Your 2026 IRMAA surcharge is based on your 2024 modified adjusted gross income. MAGI for this purpose is your adjusted gross income (Form 1040, Line 11) plus any tax-exempt interest (Form 1040, Line 2a). Municipal bond interest counts here even though it is not federally taxed.

If your 2024 joint MAGI exceeded $218,000, or your individual MAGI exceeded $109,000, you are subject to IRMAA surcharges in 2026. The higher your MAGI above those thresholds, the higher the tier and the larger the surcharge.

The full 2026 bracket tables for both filing statuses are in the companion article, Why One Good Financial Decision Can Raise Your Medicare Bill. That article also covers the annual surcharge amounts for each tier.

One more check worth making: note how far your 2024 MAGI falls above or below the nearest threshold. If you are $3,000 above the first MFJ threshold of $218,000, you are paying the full Tier 1 surcharge for the year because of that $3,000. If you are $3,000 below it, any unplanned income this year could push you over in 2028. Either position has planning implications.

What Caused Your Medicare Premium to Increase: Five IRMAA Triggers

If IRMAA is in your current bill, something in your 2024 income picture pushed you above a threshold. The most useful diagnostic question is not “what is my MAGI” but “what changed in 2024 that would not have been in a typical prior year.” The answer is almost always one of the following.

Read through these with your 2024 in mind. If you are not yet on Medicare, read them with 2026 in mind, because those decisions will determine your 2028 premium.

A Roth conversion

This is the most common unplanned IRMAA trigger. Roth conversions count as ordinary income in the year of conversion. A $100,000 conversion adds $100,000 to MAGI.

If your other income was already close to a threshold, even a modest conversion may have pushed you into a higher tier. The conversion may still have been the right long-term move. The question is whether the amount was sized with the Medicare consequence in mind.

A property or investment sale

Gains above the $500,000 primary residence exclusion for married couples count toward MAGI. Sales of second homes, rental properties, and investment accounts carry no exclusion. If a meaningful real estate or investment gain landed in 2024, especially alongside other income sources like Social Security, pension, or RMDs, the combination may have pushed MAGI above a threshold.

RMDs stacking on everything else

Required Minimum Distributions are fully taxable and count toward MAGI. When they begin at 73 and layer on top of Social Security, pension income, dividends, and interest, many households find their total MAGI higher than it ever was during their working years. RMDs also grow each year as the required percentage rises with age. If your RMDs increased in 2024, the impact flows directly into your 2026 premium.

Municipal bond interest

Tax-exempt municipal bond interest does not appear in your taxable income, but it does appear on line 2a of your Form 1040 and is added back when calculating MAGI for IRMAA. A portfolio built specifically to reduce taxable income may still be generating MAGI that pushes you above a threshold. Many households with significant municipal bond holdings discover this only after their first Medicare bill arrives.

A year-end fund distribution you did not expect

Mutual funds distribute accumulated capital gains to shareholders in November or December. These distributions are not optional and can be substantial in years when the fund realized significant gains. A household that carefully managed its income all year can find that a late December distribution tips MAGI over a threshold. If 2024 was a strong market year for your funds, check whether any distributions appear on your year-end statements that may have affected your MAGI.

If you can identify which of these applies to your 2024, you have your diagnosis. That matters because the response depends on what type of situation you are in. It may be a one-time spike that will resolve next year, a structural change that will persist, or a situation that may support an appeal.

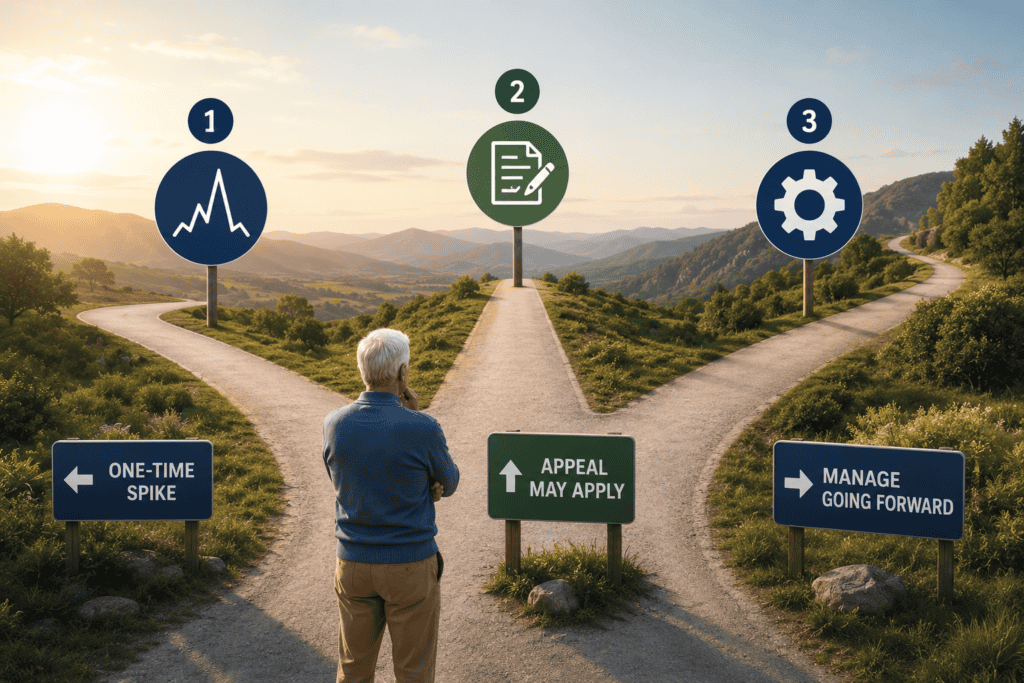

What to Do About IRMAA: Three Paths Based on Your Situation

Once you know whether IRMAA is in your bill and what caused it, you have three possible paths. Most households fall into one of them cleanly.

Path 1: One-Time Spike

Wondering if IRMAA is quietly inflating your Medicare premiums? Schedule a conversation with our team to review your situation, identify which income year is driving your surcharge, and explore strategies that may help reduce it going forward.

If the cause was a non-recurring event in 2024, a larger-than-usual Roth conversion, a property sale, a one-time distribution, your MAGI will likely be lower in 2025. That means your 2027 Medicare premium should return to a lower tier automatically once SSA processes your 2025 tax return.

You do not need to file an appeal. You do not need to take any action other than monitoring what happens to your 2025 MAGI. The more useful focus is making sure 2025 and 2026 income events are IRMAA-aware so the spike does not repeat.

Path 2: Income Dropped — Appeal May Apply

If your income is significantly lower today than the 2024 return Medicare is using, and that drop resulted from a qualifying life event, you may be able to ask Social Security to recalculate your premium using more recent income. This is done through Form SSA-44, available from the Social Security Administration at SSA.gov.

The qualifying events are: marriage, divorce or annulment, death of a spouse, retirement or stopping work, and reduction in work hours. Also qualifying: loss of income-producing property due to a disaster, loss or reduction of pension income, and receipt of an employer settlement payment from a pension plan termination.

The appeal requires documentation of the qualifying event and an estimate of your current income. It does not apply to one-time income spikes that have since passed. If you had a large Roth conversion in 2024 but your income is back to normal now, the SSA-44 process generally does not apply.

The trigger was a financial decision, not a qualifying life event. Consult a qualified professional to evaluate whether your specific situation qualifies before filing.

Path 3: Structurally Higher — Manage It Going Forward

If your MAGI is structurally above a threshold because of RMDs, pension income, Social Security, and investment distributions that are simply part of your retirement picture, IRMAA is not going away on its own. The question shifts from “how do I get out of this” to “how do I manage it intelligently going forward.”

The tools available at this stage include Qualified Charitable Distributions from your IRA after age 70½, which satisfy RMDs without increasing MAGI. They include Roth IRA withdrawals in years when you need income beyond what your mandatory distributions provide, since qualified Roth withdrawals do not increase MAGI. Annual MAGI projection before any discretionary income decisions is also part of the toolkit. The goal is to choose which bracket you land in, rather than discover it after the fact.

The goal is not to eliminate IRMAA at any cost. Sometimes paying a surcharge is the right outcome. The financial decisions that caused it, whether Roth conversions, property sales, or investment restructuring, may have been worth more than the Medicare cost. The goal is to make that choice deliberately rather than stumble into a higher bracket by accident.

How 2026 Income Decisions Affect Your 2028 Medicare Premium

Regardless of where you stand today, one question has immediate practical value: what income events are you planning in 2026?

Because of the two-year lookback, decisions made in 2026 will set your 2028 Medicare premium. Each major income decision this year carries a Medicare echo that arrives two years later. That applies to a Roth conversion, a property sale, or a large IRA withdrawal. The time to evaluate that echo is before the transaction, not after it becomes a line on your Medicare notice.

The practical check is straightforward. Estimate your total 2026 MAGI from all sources: Social Security, pension, RMDs, dividends, interest, capital gains, Roth conversions, and any other distributions you are planning. Compare that figure to the IRMAA threshold for your filing status. If you are close to a threshold in either direction, that is worth knowing before any discretionary income decision this year.

For households still years from Medicare, the same logic applies in reverse. The income decisions made between ages 60 and 63 are the ones that shape the first Medicare bill at 65. The planning window is not when you enroll. It is now.

“IRMAA is not a penalty for bad decisions. It is a surcharge that sometimes follows good ones made without full information. The difference between an accidental IRMAA bill and a planned one is usually a single conversation that happened before the income decision, not after.”

Langan Financial Group

What to Bring to Your Advisor: Your IRMAA Action Plan

If something in this article raised a question about your current premium or a planned income event, bring three things to your next planning conversation: your 2024 MAGI from lines 11 and 2a of your Form 1040, a list of income events you are considering for 2026, and your Medicare Initial Determination Notice if you have it. Those three items are everything needed to evaluate your current position and model the 2028 impact of planned transactions.

That is enough to evaluate your current position, model the 2028 impact of planned transactions, and determine whether an appeal, an adjustment, or a change in approach makes sense for your situation.

The free IRMAA Awareness Worksheet that accompanies this issue walks through the same diagnosis in a structured format you can complete with your tax return in hand. It includes both bracket tables, a trigger checklist for 2024 and 2026, a long-term exposure estimate, and the three questions to bring to your advisor. It is available as a free download through the link in this week’s newsletter.

Not Sure Where Your MAGI Falls or What Path Applies to You?

We work through this analysis regularly with families in and approaching retirement. A complimentary review can identify your current IRMAA position, evaluate the 2028 impact of any planned transactions, and determine whether an appeal may apply to your situation.

Schedule a Complimentary Review

Or call us at 717-288-1880

Curious how proactive income planning could affect your Medicare costs in retirement? Discover approaches used to manage IRMAA surcharges year to year — discuss your situation with an advisor who can help you understand your options before the next determination period arrives.

This article is provided for informational and educational purposes only and does not constitute investment, tax, legal, or Medicare planning advice. All investing involves risk, including potential loss of principal. Individual results will vary.

IRMAA thresholds and surcharge amounts reflect the 2026 Medicare IRMAA amounts based on 2024 MAGI, as published in the CMS 2026 Medicare Parts A and B Premiums and Deductibles announcement and confirmed by the SSA IRMAA Sliding Scale Tables. The standard 2026 Part B premium of $202.90 per month is sourced from CMS. IRMAA brackets and surcharge amounts are adjusted annually by CMS and may change in future years.

Any references to IRMAA surcharge amounts are for educational purposes only and do not constitute projections or guarantees of future Medicare costs. The primary home sale gain exclusion of $500,000 for married couples and $250,000 for single filers reflects current law and may change. Form SSA-44 information is provided for general educational purposes.

Eligibility for a life-changing event appeal depends on individual circumstances. Not all situations qualify, and the appeal process does not apply to one-time income spikes that have since returned to lower levels. Consult Social Security Administration resources or a qualified professional before filing.

The MAGI calculation reflects IRS and SSA methodology current as of the date of publication. Part D IRMAA surcharges are paid directly to Medicare, not to your drug plan or insurer, and may be deducted from your Social Security benefit or billed separately. Please consult a qualified financial, tax, or Medicare planning professional before making any decisions based on information in this article.

Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.