Key Takeaways

- Start long-term care planning before health declines, as 33% of applicants in their 60s get declined.

- Run actual math on self-funding costs before assuming personal savings will cover long-term care.

- Medicaid’s five-year lookback period means delaying asset protection strategies reduces your available options.

- Evaluate which funding options remain open to you before comparing specific long-term care products.

- Pennsylvania families should assess health, age, assets, and timing before choosing any care funding approach.

Understanding why long-term care planning matters is not the hard part. Most Pennsylvania families who have watched a parent go through a care event already know what is at stake. The hard part is knowing what to actually do about it — which approach fits your situation, and whether some of your options have already quietly closed.

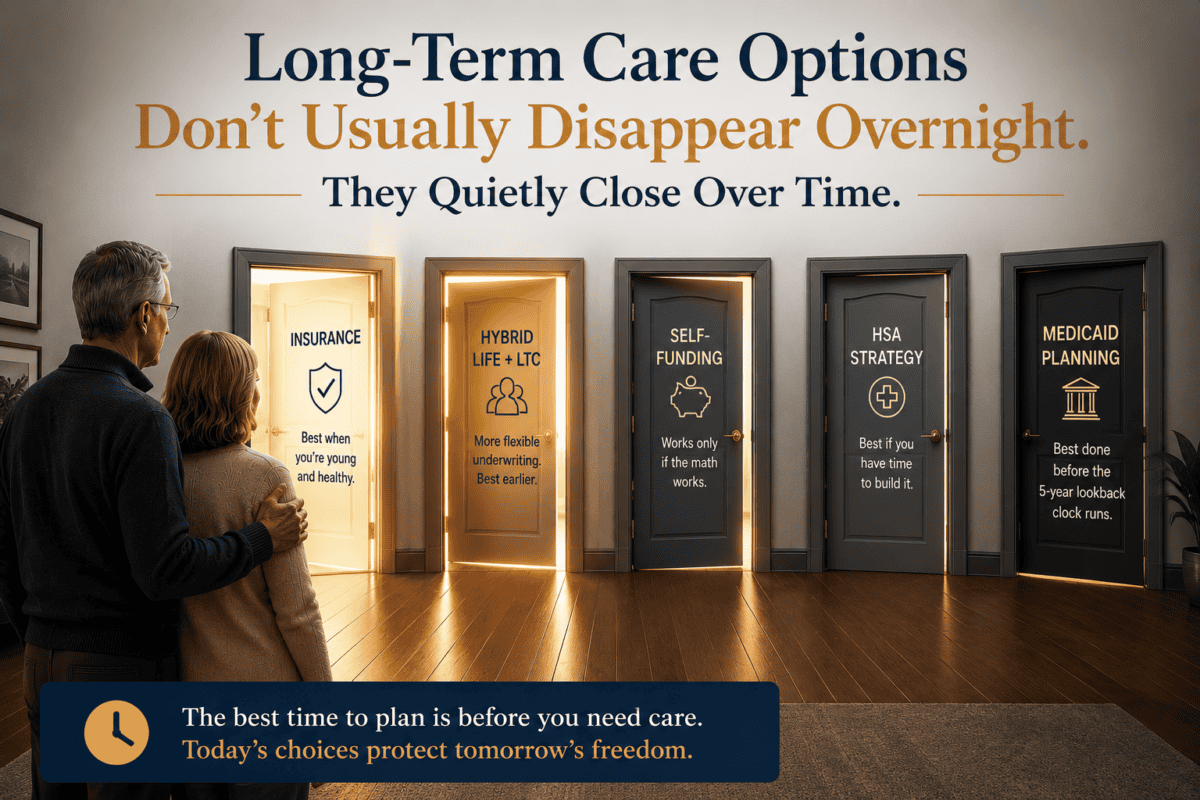

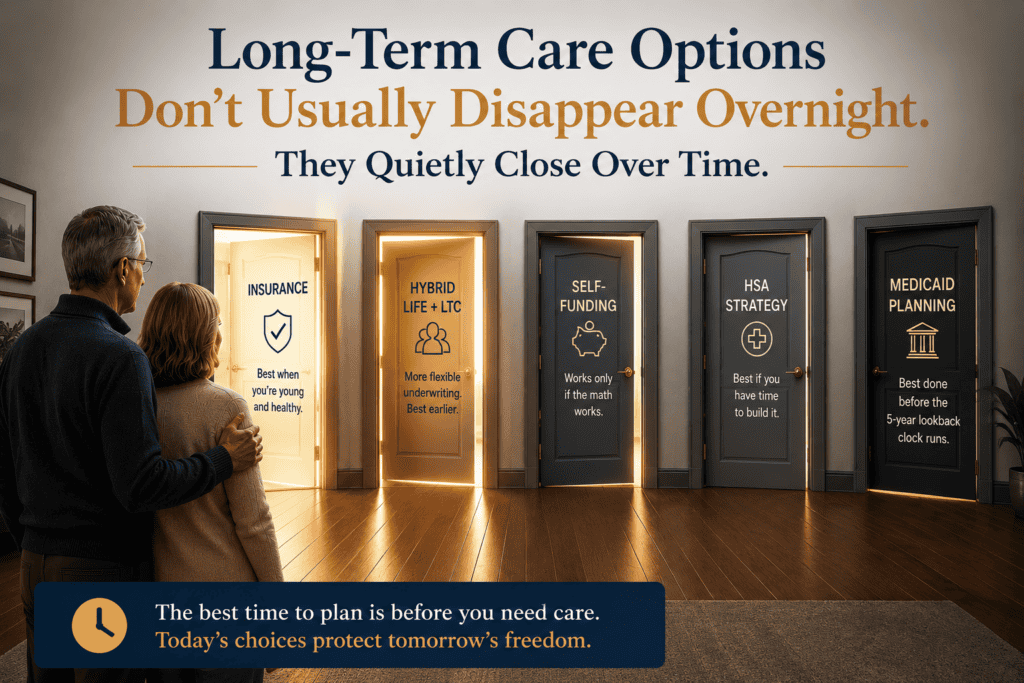

There are five realistic ways Pennsylvania families fund long-term care. Each one fits a different situation. Some require good health to access.

Some require a lump sum. Some require time — specifically, time before the Medicaid five-year lookback clock makes certain strategies less effective. And one option, self-funding, only works if you have run the actual math rather than simply assuming savings will handle it.

Start with four questions. The answers will tell you which options are still open to you before you spend time evaluating any of them.

Four Questions That Determine Which Options Are Still Available

Most people approach long-term care planning by asking which product sounds right. The better starting point is understanding which options still apply to your situation.

Question 1: How old are you, and how is your health?

Long-term care insurance — both traditional policies and hybrid policies — requires medical underwriting. The insurance company reviews your health before agreeing to cover you. Conditions that may affect eligibility include insulin-dependent diabetes, a recent stroke or heart attack, Parkinson’s disease, certain cancers within the past several years, significant cognitive issues, and some mental health diagnoses. According to AALTCI data, approximately 21 percent of applicants in their early 60s are declined — rising to roughly 33 percent for those applying at ages 65 to 69.

If you are in good health and under 65, insurance options are likely still available and worth pricing. If you have significant health issues, traditional LTC insurance may no longer be accessible — but hybrid policies often have more flexible underwriting and may still be an option. Options 3, 4, and 5 remain available regardless of health.

Question 2: Could you realistically self-fund a three-year care event?

This question requires three steps, not one.

Step 1 — Estimate your likely cost. Choose the care setting most realistic for your situation. Three years at the Harrisburg or York area nursing home average runs approximately $370,000 to $380,000 at current rates. Three years of Pennsylvania assisted living runs approximately $165,000 to $200,000.

Step 2 — Run the percentage test. Divide that estimated cost by your total investable assets, not including your home. If the result is more than 25 percent of your portfolio, a three-year care event carries meaningful risk to your retirement income. If it exceeds 50 percent, self-funding without a dedicated reserve is likely not a sound strategy. These are planning guidelines, not hard rules — your specific situation may differ.

Step 3 — Add the market stress test. Now assume markets drop 20 to 30 percent in the same year care begins. Add that portfolio loss to the care cost. What does the financial picture look like for the spouse who remains at home? If that scenario is uncomfortable to think through, it is worth addressing before it happens.

If you have more than $2 million in liquid assets and the percentage test comes in below 20 percent even under market stress, self-funding may deserve consideration with a proper plan. For most Pennsylvania families in the $500,000 to $1.5 million range, a three-year care event represents a significant share of the portfolio — and some form of coverage or planning makes more sense.

Question 3: What does your Medicaid timeline look like?

When someone applies for Medicaid in Pennsylvania, the state reviews all financial transactions from the 60 months prior to the application date. Gifts to children, transfers to family members, assets moved for less than fair value — any of these within that window may trigger a penalty the family covers out of pocket.

Ask yourself: Have you helped a child with a down payment? Added a family member to a deed? Transferred money to a joint account?

Made any significant gifts? If so, those transactions may already be inside the lookback window for a care event in the next few years.

If you have made significant transfers in the past five years, talking to an elder law attorney now gives you the best chance of protecting what remains. If your record is clean, understanding the rules early — before any future transfers — keeps all options open.

Question 4: Does your spouse’s financial security depend on yours?

If a care event began tomorrow and required three or more years in a Pennsylvania nursing home, what would your spouse live on? Pennsylvania’s Community Spouse Resource Allowance protects up to $162,660 in assets for the at-home spouse in 2026, plus a monthly income allowance of up to $4,066.50. Add up your spouse’s realistic monthly expenses — housing, utilities, food, transportation, healthcare. Does the protected amount cover that realistically and for as long as needed?

For couples where both spouses depend on a shared asset base, a care event changes both financial pictures. This increases the value of strategies that ring-fence assets — whether through insurance, trust structures, or Medicaid-exempt repositioning — and changes how self-funding math works.

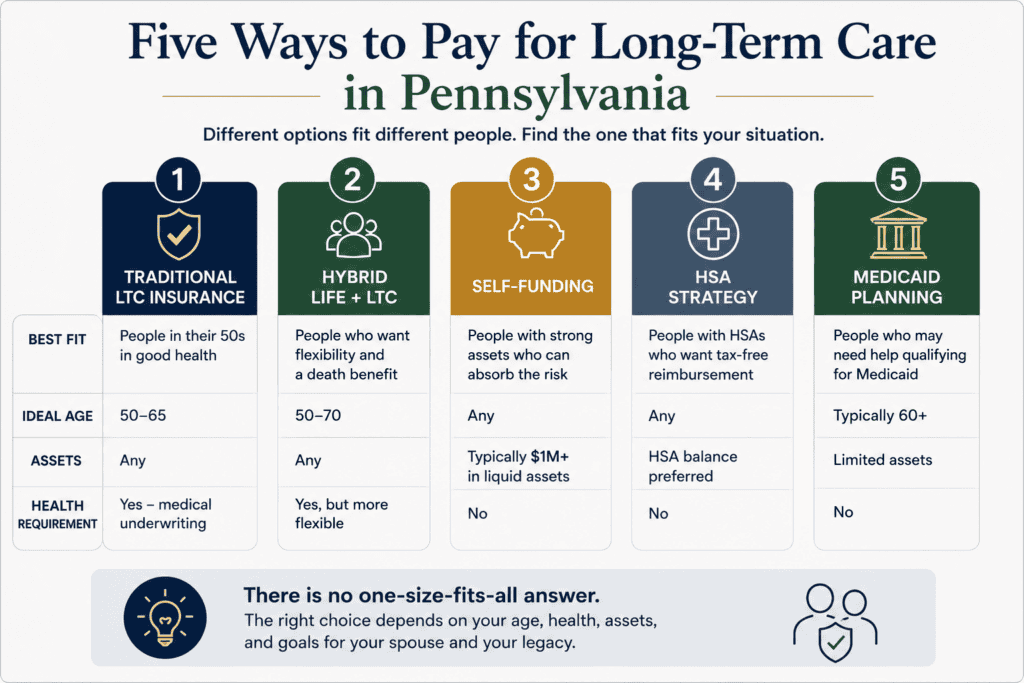

The Five Options — With the History Most Advisors Skip

Best fit: People in their 50s in good health who want dedicated, straightforward LTC coverage with a clear benefit structure.

Not ideal for: People with significant health conditions, those past their mid-60s without prior coverage, or anyone not prepared for premiums that are not guaranteed to stay level.

Key watch-out: Premiums have increased substantially on older policies. New policies carry better pricing models — but premiums are still not guaranteed. Understand this before purchasing.

Traditional LTC insurance pays a daily or monthly benefit when you meet the benefit trigger — needing help with at least two of the six Activities of Daily Living, or having a documented cognitive impairment. You choose the daily benefit amount, how long benefits last, and the elimination period (the waiting time before the policy pays, typically 90 days).

The History Worth Knowing

The traditional LTC insurance market went through a significant pricing crisis over the past 20 years. Insurers originally priced these policies on actuarial assumptions that proved too optimistic — people lived longer, stayed on claim longer, and fewer let policies lapse than expected. As losses mounted, many carriers raised premiums substantially or exited the market entirely. The number of companies selling individual LTC policies fell from more than 100 to fewer than a dozen.

New policies priced and sold since approximately 2014 are built on far better actuarial data. The Society of Actuaries has estimated that policies under today’s pricing models carry only about a 10 percent probability of needing any rate increase — and if one were needed, it would likely be modest. Pennsylvania has also adopted NAIC Long-Term Care Insurance Rate Stability Rules, which make it harder for insurers to receive state approval for rate increases on policies issued here. Premiums are still not guaranteed to stay level forever — but the product available today is not the same as what caused problems for families in the 2000s and 2010s.

The Pennsylvania Partnership Program: A Benefit Most Buyers Miss

Pennsylvania participates in the federal Long-Term Care Insurance Partnership Program. Qualifying Partnership policies link your LTC insurance directly to Pennsylvania Medicaid: every dollar the policy pays in benefits protects one additional dollar of your personal assets from Medicaid spend-down, dollar for dollar. If a Partnership-qualified policy pays out $300,000 in benefits before it is exhausted, you can apply for Medicaid and protect an additional $300,000 in assets above the standard Medicaid limit. Partnership-qualified policies also protect those assets from Pennsylvania estate recovery after death.

Not every LTC policy sold in Pennsylvania is Partnership-qualified. Ask specifically whether the policy you are considering qualifies before purchasing. Inflation protection is required for Partnership qualification — which also helps ensure your benefits keep pace with rising care costs over time.

How to Make Coverage More Affordable

If the premium cost in the companion article feels out of reach, there are design levers that reduce it significantly without eliminating meaningful protection. A three-year benefit period instead of an unlimited one cuts the premium substantially — and three years covers the average care duration. A 180-day elimination period instead of 90 days reduces the premium further.

A slightly smaller daily benefit amount also helps. The goal is not maximum coverage. It is coverage that is meaningful, sustainable, and actually purchased.

What to Look For When Comparing Policies

Benefit triggers, daily benefit amount, benefit period, inflation protection, elimination period, Partnership qualification, and the carrier’s financial strength rating. Compare at least two or three carriers. If you are declined for traditional coverage due to health, ask about hybrid policies — they often have different underwriting standards.

Best fit: People with a lump sum available who want coverage that serves two purposes — LTC protection plus a death benefit if care is never needed.

Not ideal for: People who need that lump sum for monthly income, or who have not compared the specific LTC benefit structure carefully against a traditional policy.

Key watch-out: More complex than traditional LTC insurance. Review the benefit triggers, daily benefit amount, and inflation provisions carefully. Not all hybrid policies are equivalent.

Hybrid policies combine a life insurance death benefit with long-term care coverage. If care is needed, the policy pays for it — typically by accelerating the death benefit. If care is never needed, the full death benefit passes to your beneficiaries. This eliminates the concern that decades of premiums are spent on a benefit never collected.

These policies typically require a lump sum or limited-pay premium. A single payment, or payments spread over ten years, funds both protections simultaneously. Common funding sources include a 401(k) rollover, a maturing CD, or savings not earmarked for income. For couples, shared benefit pool structures are available — one combined benefit account either spouse can draw from, which can be more efficient than two separate policies.

Hybrid policies also tend to have more flexible underwriting than traditional LTC insurance in some cases, which is relevant for people who have been declined for traditional coverage or who have health conditions that create uncertainty about qualifying. Benefits are generally received income tax-free.

Best fit: Households with $2 million or more in liquid assets, a specific earmarked reserve for care costs, and a withdrawal plan that accounts for market timing risk.

Wondering which long-term care funding options are still open to you? Your health, age, and assets determine what strategies remain available — and some windows close faster than most families expect. Schedule a conversation with a Langan Financial Group advisor to explore which approaches fit your situation before your choices narrow.

Not ideal for: Anyone whose plan is simply “we have savings, we will pay when the time comes.” That is an assumption, not a plan.

Key watch-out: Care events do not wait for favorable market conditions. A significant market decline combined with concurrent care costs can erode a portfolio far faster than most plans anticipate.

Self-funding is a deliberate strategy — not a default. Families who navigate it successfully have earmarked a dedicated reserve not tied to equity markets, know their specific cost estimate, and have a withdrawal plan that handles both normal retirement income and elevated care costs at the same time.

What makes it fail is the passive version: “we have enough money, we will pay when the time comes.” A sudden care event with no earmarked reserve means liquidating whatever is available, potentially at the wrong time, disrupting income planning, and creating tax consequences that compound the financial stress.

A couple with $1.4 million in retirement savings decides to self-fund without a dedicated reserve. Three years of nursing home care in Pennsylvania costs approximately $380,000. Markets decline 25 percent in the same period.

The combination of care costs and portfolio losses may reduce their assets by more than 50 percent, leaving the at-home spouse in a significantly different financial position than the plan assumed. Individual results vary. This is for planning illustration only.

Approximately two-thirds of nursing home residents in Pennsylvania are covered by Medicaid at some point. This includes many families who entered a facility with meaningful assets and never expected Medicaid to become relevant. Care is expensive enough and long enough in duration that it exhausts more portfolios than families expect. Self-funding works for some households — with honest math, a specific plan, and a dedicated reserve.

Best fit: Pre-retirees in their late 50s to early 60s with an HSA-eligible plan who want to build a tax-advantaged balance specifically for future LTC insurance premiums.

Not ideal for: Anyone already enrolled in Medicare — contributions stop the month Medicare begins. This is a bridge tool, not a standalone strategy.

Key watch-out: The contribution window closes at Medicare enrollment. Retroactive Part A coverage can create earlier cutoffs than expected. Coordinate timing carefully.

An HSA lets you contribute pre-tax dollars and withdraw them tax-free for qualified medical expenses — including qualified long-term care insurance premiums up to IRS age-based annual limits. The 2026 contribution limits are $4,400 for self-only coverage and $8,750 for family coverage. People age 55 and older who are not yet on Medicare can add a $1,000 catch-up contribution. Both spouses can contribute the catch-up if both are 55 or older and not yet on Medicare, but each must have their own separate HSA.

When used intentionally alongside Option 1 or Option 2, the HSA reduces the after-tax cost of coverage. You contribute pre-tax, withdraw tax-free for a qualified LTC premium, and effectively pay that cost with money that never faced income tax. For someone in the 22 or 24 percent federal bracket, that meaningfully changes the real cost of coverage.

Also effective in 2026 — under the SECURE 2.0 Act, participants in qualifying employer-sponsored retirement plans such as 401(k) and 403(b) plans may withdraw up to $2,600 per year specifically to pay LTC insurance premiums, penalty-free (though still subject to income tax). Worth asking your plan administrator about if HSA contributions are not available to you.

Best fit: Every Pennsylvania family over 60 should understand these rules. Most actionable for people with significant home equity or retirement accounts, anyone who has made large gifts in the past five years, and anyone past the age where insurance underwriting is realistic.

Not ideal for: This is not a do-it-yourself strategy. Pennsylvania’s Medicaid rules are specific and nuanced.

Key watch-out: The five-year lookback clock runs backward from the Medicaid application date — covering all transactions in the prior 60 months. Any planning done today begins that window. Earlier is always better.

Pennsylvania Medicaid planning is legal asset protection within the rules of the state’s Medicaid program. It is not about hiding assets. It is about understanding which assets are already exempt under Pennsylvania law, which transfer strategies comply with the rules, and how to use the protections the state already provides before a care event makes them unavailable.

What Pennsylvania Law Already Protects

Pennsylvania’s exempt assets include the primary residence under the following conditions: the applicant intends to return home, a spouse currently lives in the home, or a qualifying caregiver child who has lived in the home for at least two years before institutionalization and provided care that delayed nursing home placement. A sibling who has an equity interest in the home and lived there for at least one year before the applicant entered a facility may also qualify. One vehicle, personal property, and prepaid funeral arrangements are also generally exempt.

Important: the home exemption does not survive death automatically. Pennsylvania may file an estate recovery claim against the home after the Medicaid recipient passes away, unless proper advance planning protected it. An elder law attorney with Pennsylvania experience can explain which trust structures and asset repositioning strategies are available in your situation.

Approximately two-thirds of nursing home residents in Pennsylvania are covered by Medicaid at some point during their stay. Understanding the rules before a care event is what determines whether a family has options — or discovers the rules too late to use them.

The Tax Advantages Most Families Miss

Long-term care insurance comes with significant tax advantages that rarely get discussed clearly. Two mechanisms apply depending on how you pay for coverage.

Premiums paid for a tax-qualified LTC policy may be counted as a medical expense for itemized deduction purposes, up to IRS age-based limits. Medical expenses must exceed 7.5 percent of your adjusted gross income to be deductible on Schedule A. HSA funds can pay those same premiums tax-free, up to the same age-based limits, with no requirement to itemize — often the more practical route for working pre-retirees who take the standard deduction.

Source: IRS Rev. Proc. 2025-32, Section 4.27.

2026 figures per AALTCI. Limits are per insured person. A married couple applies each spouse’s limit separately based on their individual age.

HSA withdrawals are tax-free for qualified LTC premiums up to these limits. Itemized deductions require medical expenses to exceed 7.5% of AGI. Consult a tax professional for your situation.

A married couple where both spouses are between 61 and 70 could use HSA funds to pay up to $9,920 in combined LTC insurance premiums tax-free annually. Most families in that situation are not taking advantage of it.

Benefits received from a tax-qualified long-term care policy are also generally income tax-free. That creates a tax advantage at both ends — premiums paid with tax-advantaged dollars, and benefits received without tax.

If a Parent’s Care Situation Is Happening Right Now

Planning ahead is ideal. When care is already underway, the timeline compresses and the priorities shift. Three things matter most immediately.

1. Do not move money or transfer assets without an elder law attorney first. When someone applies for Medicaid, Pennsylvania reviews all financial transactions from the prior 60 months. Any transfer in that window may trigger a penalty the family covers out of pocket before Medicaid begins paying.

2. Learn what the at-home spouse is legally entitled to keep. Pennsylvania protects up to $162,660 in assets for the community spouse in 2026, plus a monthly income allowance of up to $4,066.50 per month. Most families do not know these numbers until they need them.

3. Use this moment to review your own plan. The families who handle this best are the ones who watch a parent’s care event and immediately apply what they learn to their own situation. Call 717-288-1880 or visit langanfinancialgroup.com/get-started-today

Quick Reference: All Five Options at a Glance

Use this to identify which options are most likely still available to you, then return to the relevant section above for the full detail.

General planning reference only. Eligibility, costs, and timing vary by individual health, assets, and circumstances. Consult a qualified financial, legal, or tax professional before making decisions.

Three Steps Worth Taking This Week

Step 1: Run the self-funding math. Use the three-step calculation from Question 2 above. Write down your actual number — the estimated cost of three years of care at the care setting most realistic for your situation, divided by your investable assets, then stress-tested against a 25 percent market decline. If you have never seen that number, you need to see it before evaluating any strategy.

Step 2: Check the five-year lookback window. Think through any significant financial gifts or asset transfers made in the past five years. A down payment help to a child, a large gift, money moved to a joint account. If any of those are present, an elder law attorney conversation should happen sooner rather than later.

Curious how Pennsylvania families are approaching long-term care costs without derailing their retirement plans? Download our complimentary guide to discover the five funding methods covered in this issue — and the key questions to ask before comparing any specific products. Get the resource and discuss your situation with our team at your own pace.

Step 3: Identify your one or two most likely options. Based on your age, health, assets, and the quick reference table, identify which options are still realistically available. Then have a specific conversation with a qualified advisor about whether they fit into your overall retirement plan — including the tax implications, income needs, and your spouse’s long-term security.

“The families who handle long-term care best are not the ones with the most money. They are the ones who had the conversation while they still had choices.”

Long-term care does not require a perfect answer. It requires an honest look at which options are still open, a realistic estimate of what you are protecting against, and a decision made on your terms — not in a hospital waiting room.

We help Pennsylvania families in the Harrisburg, York, and Lancaster areas work through long-term care planning as part of a coordinated retirement plan. Most conversations take less than 20 minutes.

This article is for educational purposes only and does not constitute investment, tax, or legal advice. Long-term care insurance options, availability, and premiums vary by individual health, age, carrier, and coverage selection. Premium history referenced reflects policies issued prior to 2014; policies issued since 2014 carry different pricing profiles.

Pennsylvania Long-Term Care Insurance Partnership Program qualification requires specific policy features including inflation protection; confirm Partnership qualification with the insurer before purchasing. Tax information reflects 2026 IRS guidance and is subject to change. HSA eligibility requires enrollment in a qualifying high-deductible health plan; contributions stop at Medicare enrollment.

Pennsylvania Medicaid rules and figures are current as of 2026 and subject to change; the home exemption is subject to estate recovery absent advance planning; consult a Pennsylvania elder law attorney. The SECURE 2.0 provision applies to qualifying employer-sponsored plans only; IRA eligibility is pending IRS guidance; plan must opt in; distributions are subject to income tax. Hypothetical scenarios are for planning illustration only.

Individual results will vary. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser.

Langan Financial Group and Cambridge are not affiliated.

-

- Pennsylvania Insurance Department, Long-Term Care Partnership Program — pa.gov/agencies/insurance

- American Association for Long-Term Care Insurance (AALTCI), 2024 Price Index and 2026 Tax Limits — aaltci.org

- IRS Rev. Proc. 2025-32, Section 4.27 — 2026 LTC Insurance Premium Deduction Limits — irs.gov

- Society of Actuaries / Comfort LTC, LTC Pricing Project Nov. 2016 — comfortltc.com

- IRS Rev. Proc. 2025-19 — 2026 HSA Contribution Limits — irs.gov

- Fidelity Learning Center, 2026 HSA Contribution Limits — fidelity.com

- MedicaidLongTermCare.org, Pennsylvania Medicaid Long-Term Care 2026 — medicaidlongtermcare.org

- Marshall, Parker & Weber LLC, 2026 PA Medicaid Spousal Resource & Penalty Divisor — paelderlaw.com

- U.S. Dept. of Health and Human Services, Long-Term Care Statistics — aspe.hhs.gov

-

- CNBC, SECURE 2.0 Rule: Penalty-Free 401(k) Withdrawals for LTC Insurance, Dec. 30, 2025 — cnbc.com

- KFF Health News, “Why Long-Term Care Insurance Falls Short for So Many,” Nov. 2024 — kffhealthnews.org

- Nolo.com, When Medicaid in Pennsylvania Will Pay for a Nursing Home — nolo.com