Retirement Is Not a Number. It Is a Paycheck.

How to Stop Worrying About Your Balance and Start Understanding Your Income

Key Takeaways

- Convert your retirement savings into a monthly income estimate, not just a lump sum balance.

- Focus on predictable income streams to reduce retirement anxiety beyond portfolio size.

- A smaller balance generating reliable income beats a larger balance with no withdrawal strategy.

- Stop benchmarking your savings against generic magazine targets; benchmark against your personal expenses instead.

- Retirees reporting higher confidence share one trait: they receive income as a regular, predictable stream.

The Question Nobody Answers Clearly

There is a question that keeps more people awake at night than any market headline, tax change, or inflation report.

“Can I actually retire?”

Not “should I rebalance my portfolio.” Not “when should I claim Social Security.” Those are important questions, but they come later. The 2am question is simpler and heavier than all of those.

“If I stop working, will I be okay?”

Most people carry this question quietly for years. They check their 401(k) balance. They glance at retirement calculators online.

They compare their number to whatever figure a magazine or a coworker mentioned. And almost always, the answer they get back is the same: a single lump sum, a target to hit or miss.

Here is the problem with that answer. It does not actually tell you whether you can retire. It tells you what you have saved. Those are two different things.

Why the Lump Sum Never Feels Like Enough

A person with $1.2 million in retirement savings might feel anxious. A different person with $800,000 might feel calm. The difference has almost nothing to do with the dollar amount. It has everything to do with whether they have turned that number into something they can understand.

A lump sum sitting in an account feels like a countdown. Every withdrawal makes it smaller. Every market dip makes it scarier.

Every birthday makes the math feel tighter. The natural response to a shrinking number, no matter how large it started, is worry.

Research from the Employee Benefit Research Institute consistently shows that retirees who receive income as a regular, predictable stream tend to report higher confidence than retirees with the same total wealth held as a lump sum. The money is the same. The experience of it is completely different.

This is not a trick. It is a structural insight. The way you see your money shapes how you feel about your money. And how you feel about it shapes the decisions you make with it.

The Shift That Changes Everything

Retirement is not a savings number. It is a paycheck replacement plan.

During your working years, you receive a paycheck. It arrives on a schedule. It covers your bills.

If it is large enough, there is money left over for the life you want. You do not wake up each morning wondering whether your employer will still exist tomorrow. The paycheck provides structure, and structure provides calm.

Retirement works the same way, or it should. The difference is that instead of one paycheck from one employer, your income comes from multiple sources. Social Security.

A pension, if you have one. Withdrawals from savings. Each source has different rules.

Some are guaranteed for life. Some adjust for inflation. Some depend on markets.

Some are taxed differently than others.

The families who feel most confident in retirement are not the ones with the largest portfolios. They are the ones who know exactly what comes in every month, where it comes from, and whether it covers the life they want to live.

That clarity is the paycheck. And building it is the single most valuable thing you can do before or during retirement.

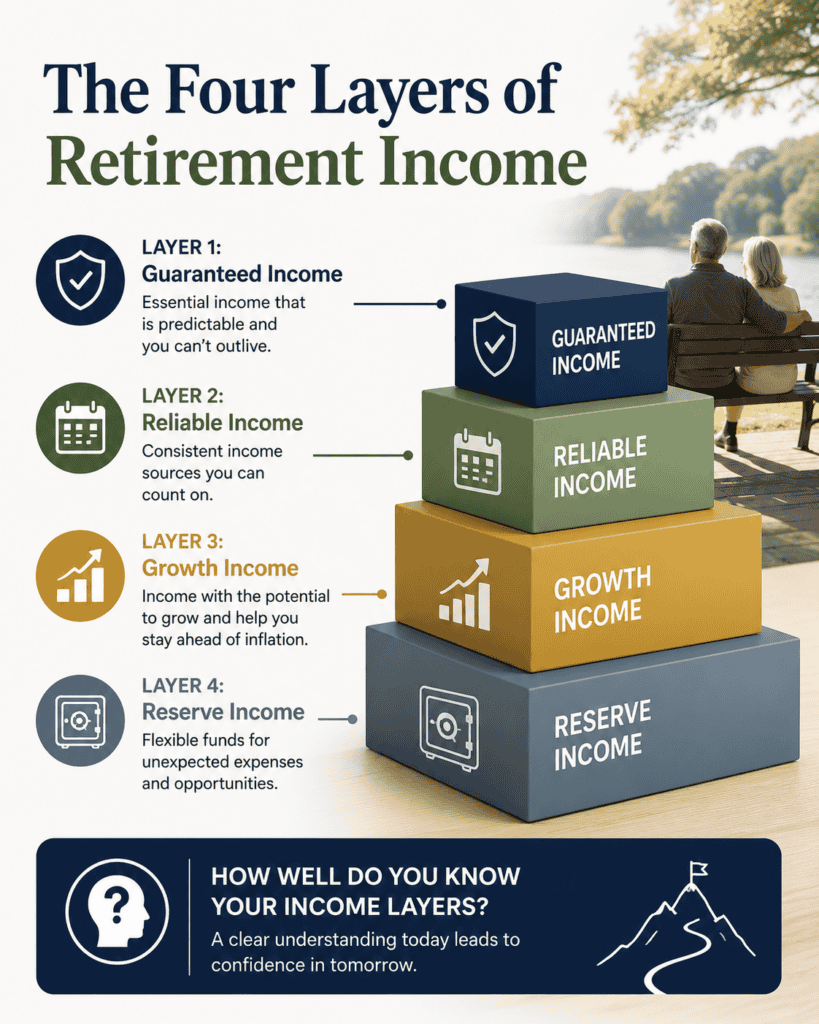

The Four Layers of Retirement Income

Think of your retirement income as four layers, each with a different job. The goal is not to grow any single layer as large as possible. It is to make all four work together.

Layer 1: Guaranteed Income

This is income that arrives every month no matter what markets do. For most families, it includes Social Security and possibly a pension or annuity.

Social Security is the most important asset most retirees own. According to a 2025 Pew Research Center analysis, 63% of beneficiaries say Social Security accounts for at least half their income. For roughly 27% of beneficiaries, it is their only source of income. It is adjusted for inflation, lasts for life, and continues (at a reduced level) for a surviving spouse.

A pension, for those who have one, adds a second layer of guaranteed monthly income. The important details are whether it adjusts for inflation (most private pensions do not) and whether it continues to a surviving spouse.

If you are in your early 50s: Your guaranteed income layer is still being built. Every year of work increases your Social Security benefit. Every year you delay claiming past full retirement age (67 for those born in 1960 or later) adds 8% per year to your benefit, up to age 70. That 8% is set by federal law, indexed to inflation, and guaranteed for life.

If you are in your early 60s: This is the claiming decision window. The choice of when to claim Social Security is one of the most important financial decisions you will make. It sets your check, your spouse’s survivor benefit, affects how much of your benefit is taxed, and interacts with Medicare premiums. This decision deserves more than a five-minute conversation.

If you are already receiving benefits: Your guaranteed income layer is in place. The question now is whether it covers your essential expenses. If it does, your portfolio serves a different and less stressful purpose than you may realize.

Layer 2: Reliable Income

This is income that is not technically guaranteed but is structured to be steady. It includes interest from bonds, CDs, and Treasury securities. It includes dividends from established companies with long histories of consistent payments. It includes structured withdrawal plans that pull a set amount from savings on a schedule.

In the current rate environment, this layer has become more attractive. With the Federal Reserve holding rates at 3.50% to 3.75% and no cuts expected until 2027, yields on CDs, Treasury bills, and high-quality bonds are higher than they have been in over 15 years.

If you are in your late 50s: If you are saving in a money market or savings account, the current rate environment is working in your favor. The question is whether your holdings are set up to take advantage of it.

If you are retired: Reviewing what you hold, what yields you earn, and when each holding matures is a practical step that often improves monthly cash flow without changing your broader investment strategy.

Layer 3: Growth Income

This is income generated by your portfolio’s long-term investments, typically stocks and stock funds. It is not steady month to month, but over longer periods, it provides the growth that helps your income keep pace with inflation across a 20- or 30-year retirement.

This is the layer that makes headlines. It is also the layer most likely to trigger emotional decisions. Research from DALBAR’s 2025 Quantitative Analysis of Investor Behavior found that in 2024, the average equity investor underperformed the market by 8.48 percentage points, not because of poor fund selection, but because of poorly timed buying and selling decisions driven by emotion.

Wondering what your retirement balance actually looks like as a monthly paycheck? Schedule a conversation with Langan Financial Group to explore how your savings could translate into a predictable income stream built around your real expenses, not a generic magazine target.

The key insight for both retirees and pre-retirees: the growth layer should not be the source of monthly income for essential expenses. If your grocery bill, mortgage, and healthcare costs depend on your stock portfolio performing well this quarter, your plan has a structural gap.

When guaranteed and reliable income cover your essential expenses, the growth layer is freed to do what it does best: grow over time without being disrupted by forced selling during down markets. That is the structural advantage that separates a stressful retirement from a confident one.

If you are in your late 50s and early 60s: The decade before retirement is when the relationship between your growth layer and your income layers should start to shift. This does not mean abandoning stocks. It means making sure you are not planning to depend on stock returns to pay next month’s bills on day one of retirement.

If you are retired: If the spring 2026 market swings made you think about selling, that feeling was information about your structure. If your essential expenses are covered by layers one and two, a market drop changes your statement but not your lifestyle. If they are not, that is the gap to close.

Layer 4: Reserve Income

This is money you hope to never need but that exists as a backstop. It includes home equity, cash value in life insurance policies, an emergency fund, and in some cases, a home equity line of credit.

Home equity is the largest reserve asset most families hold. However, home equity is only useful as retirement income if you are willing and able to access it, through downsizing, a reverse mortgage, or a line of credit.

In the current housing market, this layer deserves extra attention. Existing home sales in March fell to their lowest level in nine months, and mortgage rates have risen for five straight weeks. For families who planned to downsize as part of their retirement, the timeline for that move may be longer than expected.

If you are considering downsizing: Adding a two- to three-year buffer to your downsizing timeline in your retirement plan is a practical step given the current housing market. Planning as if the sale happens on schedule, but preparing for the possibility that it does not, gives you flexibility without requiring a change in direction.

Putting the Picture Together

When all four layers are visible on a single page, something changes. The pile of puzzle pieces becomes a picture.

A family with $1.2 million in retirement savings might see it as one large, intimidating number. Or they might see it as:

Social Security: $3,400 per month (combined household). Pension: $1,200 per month. Portfolio withdrawal at 4%: approximately $4,000 per month.

CD and bond interest: approximately $900 per month. Total monthly income: approximately $9,500.

Monthly expenses: approximately $7,800.

That family has a surplus. Their guaranteed income alone covers roughly 60% of their expenses. Their combined income exceeds their costs by $1,700 per month. The growth layer in their portfolio has room to grow without being pressured by withdrawals.

A different family with the same $1.2 million but no pension and only one Social Security check might see a very different picture. The gap between guaranteed income and essential expenses might be $3,000 per month, all of which must come from the portfolio. That is not a crisis. But it is a structure that requires more careful management and a more deliberate plan for how the portfolio generates that monthly income.

Both families have the same number on paper. Their retirement experiences are fundamentally different. The difference is not the total. It is the structure.

Hypothetical scenario: These illustrations use simplified assumptions for educational purposes and do not reflect any specific individual’s financial situation. Actual income, expenses, tax treatment, and investment returns will vary. Consult a qualified financial professional for advice specific to your circumstances.

The Pennsylvania Advantage Most Families Overlook

For families living in Pennsylvania, the retirement income picture includes a meaningful tax benefit that many overlook.

Pennsylvania does not tax Social Security benefits, pension income (after eligibility age), 401(k) distributions, or IRA withdrawals at the state level. The state’s flat income tax rate of 3.07% applies to wages and investment income, but qualified retirement distributions are exempt.

This means that for many retirees, the income flowing from layers one and two, Social Security, pensions, and retirement account withdrawals, arrives free of Pennsylvania state income tax. Over a 20- or 30-year retirement, that exemption could save a household tens of thousands of dollars compared to a neighboring state that taxes retirement income.

What to Do With This Information

If you have never built your retirement income picture across all four layers, that is the most valuable next step. The free resource in this week’s newsletter, The Retirement Paycheck Builder, walks through the process in about 30 minutes.

If you have already built your picture and the income exceeds your expenses, take a breath. You may be in better shape than you realized. The anxiety you have been carrying may come from staring at a lump sum rather than seeing the income it produces.

If you have built your picture and there is a gap, that is not a reason for alarm. It is information. A gap found now, while you still have time and flexibility, is a solvable problem. The companion article in this issue covers nine specific strategies for closing that gap, several of which are only available for a limited time.

And if the exercise raised a question you cannot answer on your own, that question is worth a conversation before decisions become permanent.

The Families Who Sleep Well

They are not the ones who saved the most. They are not the ones who picked the best-performing funds. They are the ones who turned what they have into a plan they can see, understand, and trust.

They know what comes in. They know what goes out. They know the gap, or they know there is no gap. And because they know, they spend less time worrying about headlines and more time living the retirement they worked for.

That clarity is available to anyone willing to sit down and map it out. The numbers are already there. They just need to be organized into a picture.

If something in this article helped you see your own picture more clearly, or if it raised a question about a number you have not checked, that is the conversation worth having next.

Langan Financial Group

Clear guidance. Coordinated planning. Calm decisions.

Schedule a Complimentary Conversation

Curious how retirees with similar savings build the income confidence to stop worrying and start living? Discover the strategies behind turning a portfolio into a reliable paycheck by requesting our complimentary retirement income guide from Langan Financial Group today.

langanfinancialgroup.com/get-started-today | 717-288-1880

DISCLOSURE: This article is provided for informational and educational purposes only and does not constitute investment advice, financial planning advice, tax advice, or legal advice. All investing involves risk, including potential loss of principal. Past performance is not a guarantee of future results.

The four-layer income framework described is a planning illustration and does not guarantee retirement income adequacy. Hypothetical scenarios are for illustrative purposes only and do not represent any specific individual’s experience. Actual income, expenses, tax treatment, and investment returns will vary based on individual circumstances.

Social Security benefit amounts are based on Social Security Administration formulas and vary based on earnings history, work credits, and claiming age. The 8% delayed retirement credit applies to benefits claimed after full retirement age up to age 70 and is set by federal law. DALBAR data referenced is from the 2025 Quantitative Analysis of Investor Behavior.

Pew Research Center data referenced is from 2025 analysis of Social Security beneficiary income. Pennsylvania state tax treatment of retirement income is based on current law and subject to change. Bank of America rate projections are from BofA Global Research, May 2026.

The withdrawal rate examples used are for illustrative purposes only and do not represent a recommended withdrawal strategy. Please consult a qualified financial, tax, or legal professional before making any financial decisions. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC.

Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.

Copyright 2026 Langan Financial Group. All rights reserved. | 1863 Center St., Camp Hill, PA 17011