Key Takeaways

- IRMAA surcharges begin at 9,000 single or 8,000 joint MAGI, triggering higher Medicare premiums.

- Your 2026 Medicare premium is calculated using your 2024 tax return income, creating a two-year lag.

- Roth conversions, home sales, and large distributions can unexpectedly push income past IRMAA thresholds.

- Discuss Medicare premium consequences with your advisor before completing any major financial transaction.

- IRMAA applies to both Original Medicare and Medicare Advantage plans with drug coverage.

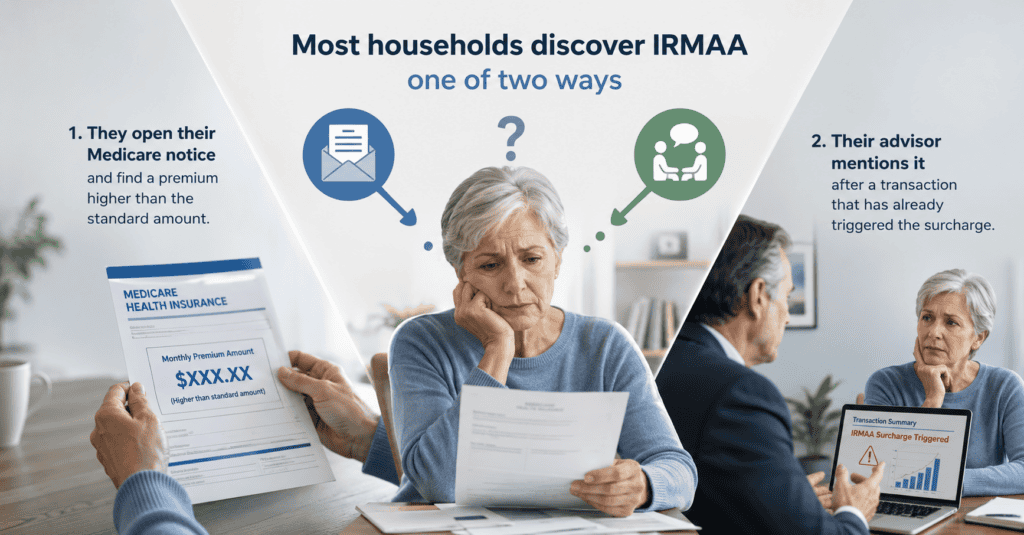

Most households discover IRMAA one of two ways. They open their Medicare notice and find a premium higher than the standard amount. Or their advisor mentions it after a transaction that has already triggered the surcharge.

Neither is ideal. The first leaves a family paying more than necessary. The second is a conversation that arrives two years too late.

The households that encounter IRMAA unexpectedly are often doing everything right. They converted to a Roth IRA in a year that made sense. They sold their home after decades of appreciation.

They took a distribution to fund a planned expense. The problem is not the decision. It is whether the Medicare consequence two years later was part of the conversation when the decision was made.

IRMAA, the Income-Related Monthly Adjustment Amount, is a Medicare surcharge that applies when your modified adjusted gross income from two years prior exceeds certain thresholds. In 2026, those thresholds begin at $109,000 for a single filer and $218,000 for a married couple filing jointly. Above those lines, surcharges are added to both Part B and Part D premiums in tiers.

The structure catches most people off guard until they encounter it. IRMAA applies whether you are enrolled in Original Medicare or a Medicare Advantage plan with drug coverage.

What Is IRMAA? How the Medicare Surcharge Works and Why It Surprises Retirees

Medicare sets your premium each year using income data from two years prior. The Social Security Administration receives your tax return from the IRS. It compares your modified adjusted gross income to that year’s IRMAA thresholds and sets your premium accordingly.

Your 2026 Medicare premium is based on your 2024 return. Your 2028 premium will be based on your 2026 return.

This gap is the source of most IRMAA surprises. A decision made in 2024 does not show up in a higher Medicare bill until January 2026. By then the income event is old news. The Medicare bill arrives as a separate letter months after the transaction, and the connection between the two is not obvious.

Modified adjusted gross income for IRMAA is not simply your taxable income. It equals your adjusted gross income from line 11 of your Form 1040, plus any tax-exempt interest from line 2a. Municipal bond interest, not subject to federal income tax, is added back for IRMAA purposes.

Many households choose tax-exempt investments specifically to reduce their tax bill. Those same investments still count toward the income figure that determines their Medicare premium.

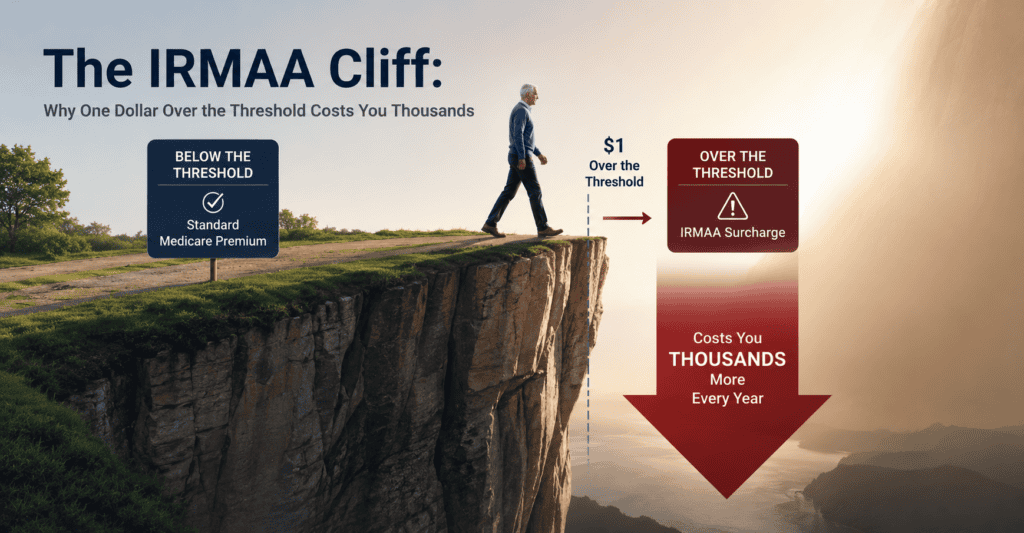

The IRMAA Cliff: Why One Dollar Over the Threshold Costs You Thousands

A regular income tax bracket is marginal. Income above the threshold is taxed at the higher rate; the rest stays at its original rate. IRMAA does not work this way.

Cross the threshold by a single dollar and the full surcharge applies to your entire Medicare premium for the whole calendar year. Both Part B and Part D are affected. Both spouses pay it.

The cliff in dollar terms

A married couple with $218,000 in 2024 MAGI pays no IRMAA surcharges on their 2026 Medicare bill. Their premium is the standard $202.90 per person per month.

A couple with $218,001 pays approximately $2,300 more per year. That is the full Tier 1 surcharge for both spouses, triggered by two dollars of income.

Source: CMS 2026 Medicare Parts A and B Premiums and Deductibles. Estimate reflects both spouses enrolled in Medicare at Tier 1. Individual results will vary.

Small amounts of income management can produce large premium differences. Staying one dollar below a threshold saves the same amount as staying $20,000 below it. The exact position of your MAGI relative to each threshold is one of the most consequential numbers in retirement planning. Most households have never calculated it.

2026 IRMAA Brackets: Medicare Surcharge Amounts for Every Income Tier

The following surcharges apply to 2026 Medicare premiums based on your 2024 MAGI. The standard Part B premium of $202.90 per person per month is added to the surcharges below. Part D surcharges are added to your individual plan premium. Source: CMS 2026 Medicare Parts A and B Premiums and Deductibles; SSA IRMAA Sliding Scale Tables.

Married Filing Jointly | Based on 2024 Joint MAGI

| 2024 Joint MAGI | Part B Surcharge/mo | Part D Surcharge/mo | Est. Extra/couple/yr |

| $218,000 or less | $0 | $0 | $0 |

| $218,001 to $274,000 | +$81.20 | +$14.50 | ~$2,300 |

| $274,001 to $342,000 | +$202.90 | +$37.10 | ~$5,760 |

| $342,001 to $410,000 | +$324.60 | +$59.70 | ~$9,220 |

| $410,001 to $750,000 | +$446.30 | +$82.30 | ~$12,690 |

| Above $750,000 | +$487.00 | +$91.00 | ~$13,870 |

Single Filers | Based on 2024 Individual MAGI

| 2024 Individual MAGI | Part B Surcharge/mo | Part D Surcharge/mo | Est. Extra/yr |

| $109,000 or less | $0 | $0 | $0 |

| $109,001 to $137,000 | +$81.20 | +$14.50 | ~$1,150 |

| $137,001 to $171,000 | +$202.90 | +$37.10 | ~$2,880 |

| $171,001 to $205,000 | +$324.60 | +$59.70 | ~$4,610 |

| $205,001 to $500,000 | +$446.30 | +$82.30 | ~$6,340 |

| Above $500,000 | +$487.00 | +$91.00 | ~$6,940 |

Annual estimates are rounded approximations for educational purposes. IRMAA brackets and surcharge amounts are adjusted annually by CMS. Part D surcharges are paid directly to Medicare, not to your drug plan or insurer, and are separate from your plan’s base premium. Individual results will vary.

How Much IRMAA Could Cost You Over a 20-Year Retirement

Monthly surcharge figures tend not to feel alarming in isolation. Eighty-one dollars per person per month sounds manageable. But IRMAA recurs every year income stays above the threshold.

A couple staying in Tier 1 for 20 years could pay approximately $46,000 in cumulative surcharges. A couple in Tier 2 for the same period could pay approximately $115,000. A couple in Tier 3 could pay approximately $184,000.

These are estimates based on current surcharge amounts, which CMS adjusts annually. Individual results will vary.

Northwestern Mutual’s 2025 Planning and Progress Study found that among millionaires’ top retirement concerns were taxes in retirement, outliving savings, and long-term care costs. IRMAA is a specific, manageable piece of that tax answer. And unlike many tax questions, it responds directly to income sequencing decisions made years before the premium bills arrive.

Five Financial Decisions That Trigger IRMAA Without Warning

None of the following are bad decisions. Each becomes an IRMAA issue when made without accounting for the Medicare consequence two years later.

Roth conversions count as ordinary income in the year of conversion. A large single-year conversion can push MAGI above an IRMAA threshold, triggering higher Medicare premiums two years later. The conversion may still be the right call.

The question is whether the amount was sized to account for the Medicare consequence alongside the tax consequence. Spreading the same total across two or three years often achieves the same long-term goal while staying below a threshold in any given year.

The Home Sale Trap

A primary residence sale may exclude up to $500,000 in gains for a married couple under current law. Gains above that exclusion count toward MAGI. Sales of second homes and investment properties carry no exclusion and can create significant one-time spikes. When a large property gain lands in the same year as Social Security, pension payments, and investment distributions, the combined total can push MAGI into a much higher tier than normal.

The RMD Stacking Trap

Required Minimum Distributions from traditional IRAs and 401(k) accounts are fully taxable and count toward MAGI. When RMDs begin at 73, they layer on top of Social Security, pension income, and investment distributions already present. The combined total often pushes MAGI higher than any single working year.

RMDs also grow each year as the required percentage rises with age. The most effective window for reducing future RMD impact is the decade before distributions start.

The Municipal Bond Trap

Tax-exempt municipal bond interest is not federally taxable, but for IRMAA purposes it is added back to AGI as part of the MAGI calculation. A household may find their visible taxable income sits comfortably below a threshold while their actual MAGI, once tax-exempt interest is added, exceeds it. This is one of the least-understood aspects of IRMAA and one of the more common sources of surprises.

The Year-End Distribution Trap

Many mutual funds distribute capital gains to shareholders in November or December. These distributions are not optional and can be substantial in a strong market year. A household can manage its income carefully all year, then find that a late December fund distribution pushes MAGI over a threshold it planned to stay below. Monitoring estimated capital gain distributions before year-end, and adjusting other income decisions accordingly, is part of IRMAA-aware planning.

Wondering if a Roth conversion or home sale could trigger higher Medicare premiums two years from now? Schedule a conversation with our team to review your income picture before your next major financial move. A proactive discussion today may help you avoid a surprise on your Medicare notice tomorrow.

What Happens When Tax Planning and Medicare Planning Don’t Talk to Each Other

Hypothetical scenario: for illustration only

Richard and Sandra retired in 2023. In 2024, their advisor recommended a $130,000 Roth conversion. The reasoning was sound: tax rates were favorable, they were between large income years, and converting would reduce future RMDs significantly. The recommendation was correct on its own terms.

What did not come up in that conversation was Medicare. The conversion pushed their joint MAGI from $162,000 to $292,000, landing them in Tier 2. In January 2026, both received Medicare notices showing higher premiums. Neither connected the bill to the 2024 conversion until consulting their tax preparer.

Had the same $130,000 been converted in two $65,000 installments across 2024 and 2025, their MAGI would have remained in Tier 1 in both years. The estimated savings over the two-year period would have been approximately $3,400. The long-term Roth benefit would have been preserved. Individual results will vary.

This scenario is hypothetical and for illustrative purposes only. It does not represent any actual client or outcome.

This is not a story about bad advice. The Roth conversion and the Medicare premium were two parts of the same decision, handled in separate conversations. When retirement planning works well, those conversations happen together.

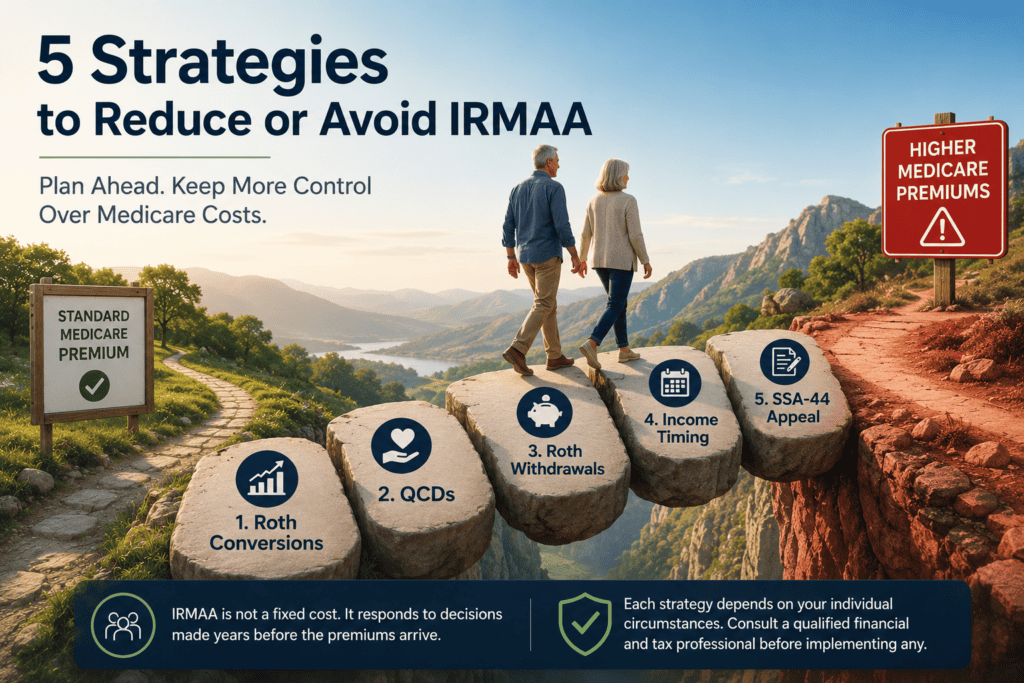

How to Reduce or Avoid IRMAA: Five Retirement Planning Strategies

IRMAA is not a fixed cost. It responds to decisions made years before the premiums arrive. Each of the following depends on individual circumstances. Please consult a qualified financial and tax professional before implementing any of them.

1. IRMAA-Aware Roth Conversion Sizing

Identify your target IRMAA tier and size each year’s conversion to keep MAGI below that threshold. This requires projecting all other income sources before determining available conversion room. The best windows are typically the years after retirement and before Social Security and RMDs begin, when other income is lowest. For households still ten or more years from Medicare, conversions can be larger because the lookback year is not yet in range.

2. Qualified Charitable Distributions

Individuals age 70½ and older can make Qualified Charitable Distributions directly from a traditional IRA to a qualified charity. These count toward the RMD but are excluded from adjusted gross income and from MAGI for IRMAA purposes. For households with charitable intentions and significant IRA balances, QCDs can meaningfully reduce MAGI without reducing how much you actually give to charity. The 2026 QCD limit is $111,000 per person, indexed for inflation annually.

3. Account Withdrawal Sequencing

Qualified Roth IRA withdrawals do not increase MAGI. Drawing from Roth accounts instead of traditional IRAs in years where you are near an IRMAA threshold can keep you below it without reducing available income. This requires having built Roth balances through earlier conversions or contributions, which is one reason the IRMAA conversation is most valuable in the decade before Medicare enrollment rather than after.

4. Timing Large Income Events

When a significant income event is controllable, its timing matters. A property sale that spans two calendar years, with proceeds recognized in separate tax years, may keep MAGI below a threshold in both years. This depends on individual transaction structure and circumstances.

This depends on individual transaction structure and circumstances. Large IRA distributions intended to fund a major purchase can sometimes be spread across two tax years for the same reason.

5. The Life-Changing Event Appeal

If your income dropped due to a qualifying life event, you may be able to request that Social Security use a more recent year’s income. Qualifying events include retirement, death of a spouse, divorce, and reduction in work hours. This is done through Form SSA-44, available from the Social Security Administration.

The appeal requires documentation of the qualifying event and an estimate of current income. For a household that retired in 2025 and is paying IRMAA based on 2023 working-year income, the savings can be substantial. Most eligible households have not used this process.

The IRMAA Widow Penalty: What Happens to Medicare Costs After a Spouse Dies

When a spouse passes away, the surviving spouse transitions from married filing jointly to single filing. This typically begins the second tax year after the death. IRMAA thresholds for single filers are roughly half those for married couples.

A couple with $200,000 in joint income paying no IRMAA surcharges may see the surviving spouse facing more than $4,600 per year in surcharges on nearly the same income. This cost arrives during the most financially and emotionally disruptive period most people will face. Individual results will vary.

IRMAA planning is couples planning. The conversions, account restructuring, and income sequencing decisions made while both spouses are alive reduce the Medicare cost the surviving spouse carries alone. A life-changing event appeal through Social Security is available when income drops due to a spouse’s death. Most surviving spouses who qualify have not used it.

Why Age 63 Is the Most Important IRMAA Planning Year Most People Miss

The standard Medicare milestones are well known: 65 for enrollment, 70 for the Social Security delay deadline, 73 for RMDs. IRMAA creates a practical checkpoint two years before Medicare itself. Your income at 63 determines your initial Medicare premium at 65. Every financial decision in retirement carries a Medicare echo two years later.

If you are 50 today, the Roth conversions and income decisions you make between now and age 63 will shape what your first Medicare bill looks like. That is the window where the most options exist and the cost of inaction is lowest.

For households between 50 and 62, the IRMAA conversation is about building the right Roth and income structure now so more options are available later. For households at 63 and 64, it is about evaluating every planned income event against the two-year lookback before executing it. For households already on Medicare, it is about annual MAGI management and the tools available to reduce unnecessary surcharges year by year.

“The households that avoid accidental IRMAA exposure are not necessarily wealthier or more sophisticated. They had someone who looked two years ahead before the transaction instead of explaining the surcharge two years after it.”

Langan Financial Group

Your Next Step: Get Your IRMAA Position Reviewed

IRMAA is manageable. It is not inevitable. The goal is not zero IRMAA at all costs.

Sometimes paying a surcharge is the right answer because the financial decision that caused it was worth more than the cost. The goal is no accidental IRMAA — surcharges that arrive from decisions made without full information.

If you are already paying IRMAA, that is useful to know. Some strategies are available to households already in a bracket, not only to those trying to avoid one. QCDs, Roth withdrawals, and the SSA-44 appeal all apply once you are in IRMAA, not only before.

If you have not reviewed where your income falls relative to the 2026 thresholds, that is a reasonable starting point. If you have income events planned for 2026 that could affect your 2028 premium, the time to evaluate that impact is before the transaction.

If something in this article raised a question about your IRMAA situation or a planned decision, that conversation is worth having before the transaction. A financial professional can look at your full income picture across the relevant years. The difference between an accidental IRMAA bill and a planned one is usually a single conversation that happened before the decision was made.

Is IRMAA Factored Into Your Retirement Income Plan?

Curious how IRMAA thresholds could affect your retirement income plan? Download our Medicare Premium Planning Guide to explore strategies for managing Modified Adjusted Gross Income across key retirement milestones. Discover approaches that may help you keep more of what you’ve worked to build.

Many plans do not account for it. A complimentary review can identify whether your current income projections and planned transactions are IRMAA-aware, and what adjustments could reduce your lifetime Medicare cost.

Schedule a Complimentary Review

Or call us at 717-288-1880

This article is provided for informational and educational purposes only and does not constitute investment, tax, legal, or Medicare planning advice. All investing involves risk, including potential loss of principal. Individual results will vary.

IRMAA thresholds and surcharge amounts reflect the 2026 Medicare IRMAA amounts based on 2024 MAGI, as published in the CMS 2026 Medicare Parts A and B Premiums and Deductibles announcement and confirmed by the SSA IRMAA Sliding Scale Tables. The standard 2026 Part B premium of $202.90 per month is sourced from CMS. Annual surcharge estimates are rounded approximations for educational purposes.

IRMAA brackets and surcharge amounts are adjusted annually by CMS and may change in future years. Cumulative cost estimates are illustrative projections based on current 2026 surcharge amounts held constant; they do not account for future bracket adjustments, income changes, or Medicare policy changes and do not constitute guarantees of future costs. The hypothetical scenario involving Richard and Sandra is fictional and for illustrative purposes only.

It does not represent any actual client or outcome. The QCD limit of $111,000 per person referenced reflects the 2026 IRS limit as confirmed by Fidelity, Vanguard, and Congress.gov CRS; verify the current year limit at IRS.gov. Form SSA-44 information is provided for general educational purposes; eligibility depends on individual circumstances.

The primary home sale gain exclusion reflects current law and may change. Northwestern Mutual 2025 Planning and Progress Study cited as a third-party research source; Langan Financial Group is not affiliated with Northwestern Mutual. Please consult a qualified financial, tax, or Medicare planning professional before making any decisions based on information in this article.

Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.