The 2026 Social Security Trustees Report came out last week. If you have seen the headlines, you have seen the number 2032 and the phrase “22% cut.” What the headlines rarely explain is what those numbers mean in plain English. They also skip what the numbers do not mean, and what the realistic range of outcomes looks like.

Key Takeaways

- The 2032 deadline signals a potential 22% benefit cut, not elimination of Social Security entirely.

- Payroll taxes and income taxes on benefits both fund Social Security’s shared trust pool.

- Higher-income retirees paying taxes on benefits directly subsidize all other retirees’ Social Security payments.

How Social Security Actually Gets Paid For

Before explaining the report, it helps to understand how Social Security is funded. Most people know about one source of money: the payroll tax. If you worked, 6.2% of your wages went to Social Security, and your employer matched it.

That money funds current retirees’ benefits. The workers paying in today support the retirees collecting today.

What fewer people know is that there is a second source of money flowing into Social Security. When higher-income retirees pay federal income tax on their Social Security benefits, a portion of that tax revenue goes back into the Social Security trust fund. Not into the general government budget. Directly back into the fund that pays benefits.

This is the part that trips people up. You may wonder: if I am paying taxes on my own benefit, am I not already taking a cut? The answer is yes, in a sense.

Taxes on your benefit do reduce what you keep. But those taxes do not go back into your personal account. They go into a shared pool that funds everyone’s benefits.

So a retiree paying income tax on their Social Security is, in part, helping fund the benefits paid to every other retiree. That is how the system was designed when Congress made benefits taxable in 1983.

Why This Matters Right Now

The One Big Beautiful Bill Act, passed in July 2025, reduced federal income taxes on Social Security benefits for many retirees. For those retirees, that meant keeping more of each check. Good news in the short term. They keep more of each benefit check.

But it also reduced the income tax revenue flowing back into the trust fund. Less money coming in means the fund runs dry a little sooner. This is one reason the projected depletion date moved from 2033 to 2032. The tax reduction benefited individual retirees today while modestly accelerating the timeline for everyone.

What the 2026 Trustees Report Actually Says

Social Security has two main trust funds. The Old-Age and Survivors Insurance fund, known as OASI, pays retirement benefits and survivor benefits. The Disability Insurance fund covers disability payments.

The 2026 Trustees Report projects that the OASI fund will run out of reserves in 2032. That is one year earlier than last year’s projection of 2033.

Running out of reserves does not mean Social Security disappears. It means the savings account runs dry. At that point, the program would pay benefits only from the payroll taxes coming in each month.

Based on current projections, those taxes would cover about 78 cents of every dollar owed. The other 22 cents would be cut from every check, automatically, for every beneficiary at the same time.

In dollars, that matters. The average Social Security retirement benefit in 2026 is approximately $2,071 per month. A 22% cut would reduce that by about $455 every month.

A couple each receiving $2,500 per month would lose roughly $1,100 combined every month. Those numbers do not include future cost-of-living increases that may occur between now and 2032, which would affect the actual dollar impact by then. But the scale is clear.

Why the Trustees Say 22% and the CBO Says 28%

The Congressional Budget Office, which reviews Social Security independently, also projects a 2032 depletion date. But its estimate of the automatic cut is 28%, not 22%. Both are working from the same program. Why the difference?

The two offices use different economic models and different assumptions about future wages, interest rates, and worker participation. Neither is wrong. They are two independent estimates of an uncertain future.

The honest answer is that no one knows the exact number. What both agree on is the direction and the approximate timeline. If Congress does not act, the cut will be somewhere in that range.

Three factors caused the projected date to move up one year. The biggest drivers were two changes in demographic assumptions. Social Security’s analysts lowered their projection for how many children the average American woman will have, from 1.90 to 1.75.

They also lowered their assumptions about future immigration. Both changes mean fewer workers paying into the program in the years ahead. Fewer workers mean less money coming in, which means the fund runs dry sooner.

The tax change from the OBBBA was a contributing factor, but the demographic assumption changes were the primary drivers of the one-year shift.

What the Report Does Not Say

The report does not predict that benefits get cut in 2032. It projects what would happen automatically if Congress takes no action at all. Those are very different statements.

Congress can change the outcome. It has done so before.

The report also does not say the situation is hopeless. The trustees list available options: raising payroll tax rates, adjusting the benefit formula, changing the retirement age, or expanding the income subject to payroll tax, among others. Each choice has political costs. But the choices exist.

Has an Automatic Cut Ever Actually Happened?

No. In the entire history of Social Security, Congress has never allowed an across-the-board automatic benefit cut to take effect. That is a meaningful fact.

The closest call was 1983. At that point, the trust fund was months away from running out of money, not years. A bipartisan deal signed by President Reagan stopped the cut.

The fix included raising payroll tax rates, gradually increasing the full retirement age, making benefits taxable for higher earners for the first time, and other changes. It extended solvency by decades.

Congress has known about the current funding gap for years and has not acted. That delay does not mean a fix is coming. The situation in 2032 would be different from 1983 in important ways.

The political environment is more divided and the timeline is less forgiving. But the historical pattern does suggest that the political cost of allowing an automatic cut tends to motivate action when the deadline is real. Whether that holds in 2032 is genuinely uncertain.

Would a Cut Affect Everyone the Same Way?

Under current law, an automatic cut would be applied equally to every beneficiary at the same percentage. A retiree receiving $1,500 per month and one receiving $4,000 per month would each lose 22%. But the impact on their lives would be very different.

For a retiree whose Social Security check covers most of their essential bills, a 22% cut is a serious problem. For a retiree whose Social Security is a supplement to a pension and other income, the same cut is painful but manageable. That difference is the whole planning question. The companion article this week gives you a way to figure out which situation applies to your household.

If Congress does act, the structure of any fix could change who is affected and how much. Many proposed solutions have included protecting lower-income retirees while asking more from higher earners. A congressional fix might not feel equal. But the automatic cut under current law would be.

What About Cost-of-Living Adjustments?

This is one of the most common questions and one of the least-answered in the coverage. The short answer: yes, Social Security’s annual cost-of-living adjustments would continue even after a cut.

If your benefit were reduced by 22%, your new, lower benefit would still receive the annual cost-of-living increase each year going forward. The cut does not freeze your benefit. It resets it to a lower starting point.

That is important because it means a reduced benefit still has inflation protection built in. It is worth knowing, even though it does not make the cut less serious in dollar terms.

What About Survivor Benefits?

Survivor benefits come from the same OASI trust fund. A 22% automatic cut would apply to survivor benefits as well as retirement benefits. For widows and widowers already living on one Social Security check instead of two, a 22% reduction hits differently.

There is no second check to cushion it. If this applies to your household, it is worth factoring into how you think about your income plan going forward.

Why 2032 Is Closer Than It Sounds, and Not as Certain as the Headlines Suggest

Six years falls inside the retirement planning window of most people reading this. A 62-year-old who has not yet claimed will be 68 when 2032 arrives. A 70-year-old already collecting benefits will be 76.

This is not a distant problem. It is close enough to plan around now.

At the same time, 2032 is not certain. The right planning position holds both realities at once. A meaningful cut is possible and worth preparing for.

Wondering how a potential 22% Social Security cut could affect your specific retirement income? Schedule a conversation with a financial advisor to explore strategies for building a retirement plan that accounts for a range of Social Security outcomes. Your situation is unique — let’s look at the numbers that actually matter for you.

A congressional fix before 2032 is also possible. The honest answer is that no one knows which will happen, and anyone who tells you they do is guessing.

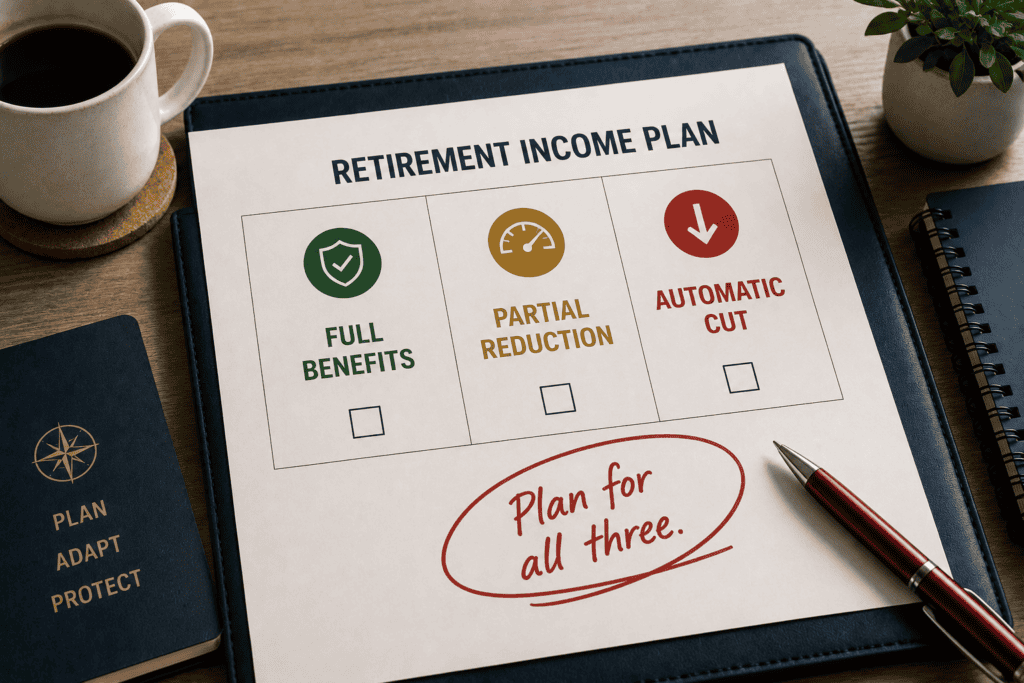

Three Realistic Scenarios and What Each Means for Planning

A well-built retirement plan should be able to handle a range of outcomes, not just one. Here are three realistic possibilities.

Scenario A: Congress Acts and Benefits Are Preserved in Full

A bipartisan fix before 2032 keeps benefits at their scheduled levels. It might include higher payroll taxes, changes to the benefit formula, a higher retirement age, or some combination. Each option has political costs, which is why action has been delayed. But when the deadline is close enough, political calculus tends to shift.

What this means for your plan: Your projected Social Security income stays as-is. No adjustment needed. The value of stress-testing for the other scenarios is knowing your plan can handle them if they arrive.

Scenario B: Congress Acts Partially and Benefits Are Modestly Reduced

A partial fix extends the fund’s life but does not fully close the gap. Benefits for some retirees, particularly higher earners, may be modestly reduced, perhaps by 5% to 15%. Many policy analysts consider this the most likely outcome if Congress acts at all.

What this means for your plan: A plan that requires every dollar of projected Social Security to cover essential bills may run short. A plan with other income sources or room to adjust spending handles this without a major problem. This is the scenario most worth modeling before 2032.

Scenario C: Congress Does Not Act and an Automatic 22% Cut Takes Effect in 2032

Most analysts consider this the least likely outcome. The political cost of letting it happen would be enormous. But it cannot be ruled out.

The average monthly benefit in 2026 is approximately $2,071. A 22% cut would reduce that by about $455 every month. A couple with two checks could lose more than $900 per month combined.

Note that cost-of-living adjustments would still apply to the reduced benefit going forward.

What this means for your plan: A household whose bills are covered mostly by Social Security would face real hardship. A household with other income sources would be much more stable. The companion article this week gives you a specific way to find out which situation applies to your household. Individual results will vary.

What a Solid Retirement Plan Does With This Uncertainty

A retirement income plan that holds up across all three scenarios has two things in common. First, it does not need 100% of projected Social Security to cover the basic monthly bills. Housing, food, utilities, insurance, healthcare, and transportation should ideally be covered by income that does not all depend on one source.

Second, it has room to absorb a reduction in one source without everything falling apart. That room may come from other income, from savings you can draw from, or from spending you have flexibility to adjust.

Neither of these requires a large portfolio. They require intentional planning. The difference between a plan that handles a Social Security reduction and one that does not is usually a conversation that happened early enough to matter. Not the size of someone’s account balance.

What to Do Based on Where You Are

The right response to this report depends on your age and your situation. Here is a plain-language framework for each group.

If You Are 50 to 62

You have time and options. This report is a prompt to look at your retirement income plan and ask one question: does this plan still work if Social Security pays 78 cents on the dollar? If yes, you are in good shape.

If not, you now know what gap to work on closing before you retire. You have years to do something about it.

One thing this report should not do is push you into claiming Social Security early out of fear. Claiming at 62 locks in a benefit that may be 25% to 30% lower than your full retirement age benefit. That reduction is permanent.

If Congress fixes the problem and you claimed early, you gave up permanent income for a risk that never arrived. If Congress does not fix it and benefits are cut, you are starting from a lower number and losing 22% of that. Early claiming does not protect you from a cut.

It compounds the problem.

If You Are 63 to 67 and Deciding When to Claim

The solvency question does not change the basic math of when to claim. Waiting past your full retirement age still adds roughly 8% per year to your benefit. And a larger starting benefit matters more in a world where a percentage cut is possible, not less.

A 22% cut applied to a $3,000 monthly benefit leaves $2,340. The same cut on a $2,000 benefit leaves $1,560. Getting the biggest possible base benefit before any reduction is generally the more careful approach.

There are exceptions. If your health or financial situation makes earlier claiming the right call for reasons that have nothing to do with the 2032 question, that is a separate conversation. Those decisions are individual and should be reviewed with someone who knows your full picture.

If You Are Already Receiving Benefits

Your benefit is the same today and stays that way unless Congress fails to act before 2032. The more useful question for you is whether your overall income plan can absorb a 10% to 22% reduction in your Social Security check. The companion article this week gives you a specific way to check that.

If the answer is yes, this report does not require you to do anything differently right now. If the answer raises a concern, that is worth a conversation with your advisor.

If the calculation reveals significant exposure, the companion article this week covers several specific strategies worth discussing with an advisor, including how to reduce your dependence ratio, which accounts to draw from first, and whether Roth conversions may make sense in the six years remaining before 2032.

The Window Is Still Open

The senators elected in November 2026 will be in office when Social Security reaches its projected date. That means the outcome of next year’s elections has real consequences for how and whether this gets resolved. The window for a negotiated fix is still open. But it is getting smaller.

None of that is a reason to panic. It is a reason to have a clear conversation about your retirement income plan before 2032 arrives rather than after. The households that tend to come through this kind of uncertainty in good shape are not the ones who predicted what Congress would do. They are the ones who built plans that could handle more than one outcome and talked through the possibilities while they still had time to make adjustments.

“The question is not whether Social Security may be reduced. The question is whether your retirement income plan is built to handle uncertainty in any single income source, including this one.”

Langan Financial Group

Your Next Step

The companion article this week, Is Your Retirement Income Plan Stress-Tested for a Social Security Reduction?, gives you a specific calculation you can complete using your own numbers. It takes about 10 minutes. It tells you which of three plan profiles fits your household, plus the one question worth bringing to your next advisor conversation.

If something here raised a question about your own plan, that conversation is worth having now. Before the uncertainty resolves itself one way or the other.

Curious how higher-income retirees can position themselves ahead of potential Social Security changes? Download our free guide to discover approaches for managing retirement income across different benefit scenarios. Knowledge is your first step toward a more resilient retirement plan.

Want to Know How Your Plan Holds Up Under Each Scenario?

We work through this kind of analysis with families approaching and in retirement on a regular basis. A complimentary review can model your income plan against all three scenarios and help you see whether any adjustments may be worth considering before 2032.

Schedule a Complimentary Review

Or call us at 717-288-1880

This article is provided for informational and educational purposes only and does not constitute investment, tax, legal, or Social Security planning advice. All investing involves risk, including potential loss of principal. Individual results will vary.

Social Security projections referenced are from the 2026 Social Security Trustees Report, published by the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds. The Congressional Budget Office projection referenced is from the CBO’s February 2026 long-term Social Security outlook. Depletion dates, automatic benefit reduction percentages, and trust fund projections are subject to change based on future economic and demographic conditions.

The average monthly benefit figure of approximately $2,071 for 2026 is sourced from the Social Security Administration. Historical 1983 reform details are sourced from the Social Security Administration’s published legislative history. The scenarios described are illustrative and do not constitute projections, predictions, or guarantees regarding future Social Security policy or benefit levels.

References to Qualified Charitable Distributions and Roth IRA withdrawals are for illustrative educational purposes only and do not constitute recommendations. Suitability depends on individual circumstances. Qualified Charitable Distribution limits and rules are subject to annual change.

Roth IRA distribution rules referenced reflect current law and may change. Please consult a qualified financial, tax, or Social Security planning professional before making any decisions based on information in this article. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC.

Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.