Key Takeaways

- Americans lost .9 billion to fraud in 2025, with investment scams accounting for nearly half.

- Adults 60+ are targeted because they answer unknown calls and have accessible retirement savings.

- AI voice cloning has created new fraud schemes that didn’t exist in meaningful form three years ago.

- Scammers exploit trust built during an era when government and banks were genuinely reliable.

- Each fraud scheme has one specific red flag and one rule that stops it.

In 2025, Americans reported $15.9 billion in fraud losses to the Federal Trade Commission. Investment scams alone generated $7.9 billion in FTC data and $8.65 billion in FBI data. Adults 60 and older filed the most complaints of any age group and suffered the most severe losses, with an average reported loss of $83,000.

These numbers do not reflect people who were careless or inattentive. They reflect people who were specifically chosen. And the reason they were chosen matters, because it has nothing to do with diminished capacity or poor judgment.

Adults in this age group answer calls from unknown numbers at significantly higher rates than younger adults. They grew up during a period when government agencies, banks, and financial institutions operated with genuine trustworthiness. That learned trust is now the mechanism that gets weaponized.

They have accessible retirement savings and home equity that can be moved quickly. They are more likely to be at home during the day when scam calls are most active. And for relationship-based schemes, the social change that often accompanies retirement or widowhood can create genuine openness to new connections.

That is not a flaw. It is human. It is also what professional criminal organizations specifically seek.

Each scheme is covered here: how it works, how AI has changed the landscape in the past two years, the specific red flag that identifies it, and the one rule that stops it. Newer schemes worth knowing that did not exist in meaningful form three years ago are also included.

Covered in this issue

- How AI has changed fraud, including voice cloning

- Investment and crypto fraud

- Government and bank impersonation

- Phishing, smishing, and account takeover

- Business email compromise and wire fraud

- Tech support and safe account scams

- Newer and fast-growing schemes

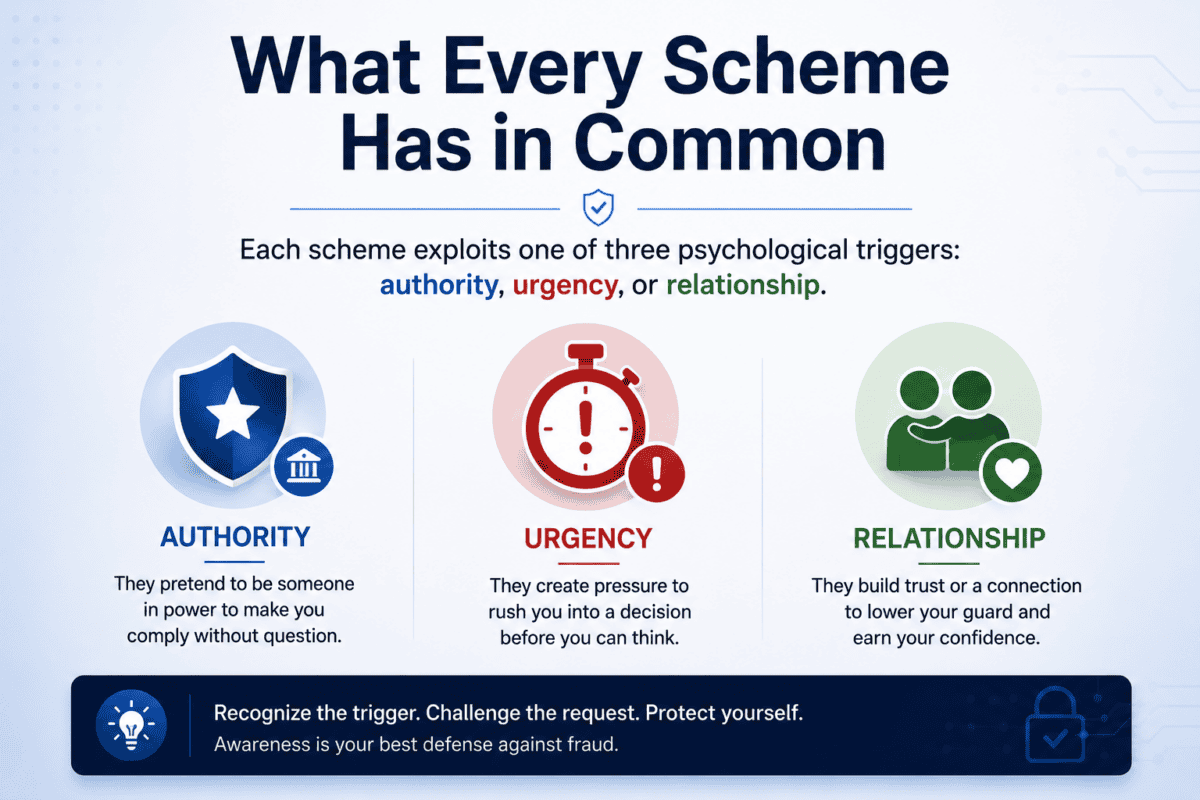

What Every Scheme Has in Common

Each scheme exploits one of three psychological triggers: authority, urgency, or relationship. Authority means the contact claims to represent an institution you trust. Urgency means you must act immediately or face a serious consequence.

Relationship means trust has been built over time before anything financial is requested. These are not accidents. They are the deliberate mechanics of the scheme.

There is also one warning sign that applies to every scheme in this article without exception: every one of them tells the victim not to consult a financial advisor. The investment fraud operator says keep this between us. The government impersonator says do not discuss this with your bank or advisor.

The tech support caller says your accounts have been compromised and your bank may be involved. The moment any contact, regardless of who they claim to be, tells you to keep something from your financial advisor, the scheme is in progress. A family code word protects against voice cloning.

This warning sign protects against everything else.

How AI Has Changed the Game

Artificial intelligence did not create financial fraud. It made every existing scheme faster, more convincing, and harder to detect. The FBI’s 2025 Internet Crime Complaint Center data logged 22,364 AI-related fraud complaints with $893 million in reported losses, and that figure likely reflects a small fraction of actual AI-assisted fraud since most victims do not know AI was involved.

AI now writes phishing emails with no typos, no broken grammar, and no obvious tells. It generates convincing investment advisor profiles with realistic photos, plausible work histories, and authentic-seeming social media presence. It creates fake video calls used in investment pitches. According to research published by Vectra AI in 2026, AI-powered scams surged more than 1,200 percent in 2025 compared to the prior year.

The most dangerous application right now is voice cloning. The technology requires 3 to 15 seconds of audio, available from any publicly posted video. According to the Hiya State of the Call 2026 report, 1 in 4 Americans received a deepfake voice call in the past 12 months. Security researchers describe this technology as having crossed the indistinguishable threshold: human listeners can no longer reliably detect a cloned voice from the real one.

The scheme most commonly built on voice cloning is the grandparent or family emergency call. A caller uses a voice clone of a grandchild or adult child to report an arrest, accident, or emergency and requests immediate cash, usually with instructions not to tell other family members. The FBI has issued multiple warnings about this variant. The FTC’s Consumer Protection Data Spotlight 2025 noted that scammers specifically harvest voice samples from social media posts by family members for use in these attacks.

The tell in a voice cloning call is not the voice. The voice may be indistinguishable. The tell is the request: secrecy from family, immediate cash, and no callback to the person directly.

A family member in a genuine emergency does not ask you to avoid calling them back on their own number. A family code word, established before any call arrives, remains the only defense that works in the moment.

One more AI-related insight worth knowing: you may have wondered how a fraud caller knew your name, your address, a family member’s name, or a partial account detail. That information very likely did not come from a data breach. It came from data broker websites that aggregate public records, social media profiles, property records, and LinkedIn pages.

The aggregated profile is inexpensive to purchase and broadly available. Understanding this demystifies the sophistication of the call. It is not magic.

It is a $30 background report combined with a professional script.

Scheme 1: Investment and Crypto Fraud

It rarely begins with an investment pitch. It begins with a contact that appears unrelated to money. A text sent to what appears to be the wrong number.

A new connection on social media who mentions strong returns in passing. A match on a dating platform who seems genuinely interested and happens to be a skilled investor. The conversation builds over days or weeks.

By the time an investment opportunity is introduced, the victim has already built what feels like a real relationship with the person presenting it.

Criminal organizations describe this process as pig butchering. The fake platform shows convincing gains. Early small withdrawals succeed, building confidence and encouraging larger deposits.

When the victim attempts a significant withdrawal, fees are demanded, taxes must be paid, or the account is suddenly frozen. The money is gone. The contact disappears.

Hypothetical scenario: for illustration only

In February, a retired professional receives a text from someone who apologizes for the wrong number but strikes up a friendly conversation. Over several weeks they speak regularly. In March, the contact mentions impressive returns on a cryptocurrency platform and offers to help set up an account.

The victim invests $5,000. The platform shows a 40 percent gain within two weeks. A small withdrawal of $1,500 goes through successfully.

Encouraged, the victim invests $40,000 more. In May, when attempting to withdraw $60,000 in apparent profits, a message appears requiring a $6,000 tax payment to release the funds. After paying, a second fee appears.

The platform becomes unreachable. The contact is gone. Total loss: $49,500.

This scenario is hypothetical and for illustrative purposes only. Individual circumstances vary. The arc described reflects patterns documented in FBI Operation Level Up case data.

Investment fraud was the largest dollar-loss category in both FTC and FBI data for 2025. The FBI’s Operation Level Up found that 77 percent of the people it proactively contacted were unaware a fraud was in progress. Through December 2025, the operation had notified more than 8,100 people. Ninety-three were referred for crisis intervention due to the severity of their losses.

The red flag

Any investment opportunity that moves to encrypted messaging, requires secrecy from family or a financial advisor, shows consistently high gains with no losses, or charges fees or taxes to release your own withdrawals.

The one rule

Never invest based on a direct message, text, or group chat. Verify any investment firm independently at investor.gov or FINRA BrokerCheck before sending money. If a legitimate investment opportunity cannot withstand that check, it is not a legitimate investment opportunity.

Scheme 2: Government and Bank Impersonation

The caller says your Social Security number has been suspended due to suspicious activity. Or the IRS has issued a warrant. Or Medicare has flagged your account for review.

Or your bank’s fraud department has detected unauthorized access and must verify your identity before someone drains your accounts. The call may appear to come from a legitimate phone number. The caller may know your name, address, and family member details.

Some calls now use AI-generated voices that sound like genuine officials.

The FTC’s 2025 data shows impersonation scams were the most reported fraud category with more than one million complaints and $3.5 billion in losses. Government impersonation reports rose 40 percent compared to the prior year. The FBI reported $797.9 million in government impersonation losses in 2025. Every variation ends the same way: move money to a safe account, pay via gift card or wire transfer, provide account codes, or stay on the line while you drive to the bank.

The red flag

Any caller creating urgency around your Social Security number, taxes, or bank accounts, particularly if they ask you to move money, provide codes, purchase gift cards, or stay on the line.

The one rule

Hang up. Call the agency or your bank using a number you already have. The IRS, Social Security Administration, and Medicare do not call demanding immediate payment. A legitimate bank fraud department does not ask you to move your money to protect it.

Scheme 3: Phishing, Smishing, and Account Takeover

Wondering if your current financial setup has blind spots that fraud schemes are designed to exploit? Schedule a conversation with our team to review your accounts, discuss protective strategies, and make sure the people you trust most know how to reach you in an emergency. A 30-minute call could be the most practical thing you do this year.

A text arrives about an undelivered package. Or an unpaid toll requiring immediate payment. Or a bank fraud alert asking you to verify your login.

Each link leads to a convincing replica of a legitimate website. When you enter your credentials, they go directly to the attacker, who uses them to access your real accounts. AI has made this significantly more dangerous in 2025 and 2026.

Phishing messages now read with perfect grammar and match the exact tone and formatting of the institutions they imitate.

The FTC reported $470 million in text-based fraud losses in 2024, more than five times the 2020 figure. The most effective early warning is channel switching. When a contact moves from text to a phone call, from a social platform to WhatsApp or encrypted chat, or from email to a wire transfer request, risk is rising. Scammers move victims across channels deliberately because each step increases emotional investment and reduces independent verification.

The red flag

Any unexpected message with a link or phone number related to a package, payment, account, or investment. Any contact that migrates across channels, text to phone, social to WhatsApp, email to wire, before asking for money or credentials.

The one rule

Never use a link or phone number from an unexpected message. Open the official app directly or type the website address yourself. If the message was legitimate, the issue will still be there when you log in through your normal channel.

Scheme 4: Business Email Compromise and Real Estate Wire Fraud

A homebuyer receives an email from what appears to be their real estate attorney. The formatting is identical to previous correspondence. It states that the title company’s banking information has changed and provides a new account number for the closing wire.

The buyer transfers the purchase funds. The attorney never sent that email. A hacker gained access to the email thread and waited for the right moment to redirect the wire.

The FBI reported $3.05 billion in business email compromise losses in 2025. The FBI’s Recovery Asset Team reports a 66 percent success rate at recovering fraudulent wire transfers when notified within hours. That rate drops significantly after the first day. This scheme is particularly relevant for anyone in or approaching retirement who may be downsizing, buying a retirement property, or helping a family member close on a home.

The red flag

Any change to wire transfer instructions arriving by email, regardless of how authentic the email appears or how familiar the sender seems.

The one rule

Before wiring any amount for a real estate transaction, call the title company or attorney using a phone number you already have on file. Verify the instructions verbally. Never confirm wiring details by email alone.

Scheme 5: Tech Support and Safe Account Scams

A pop-up appears on the computer screen stating the device has been compromised and displaying a phone number for Microsoft or Apple support. The representative who answers is calm and professional. They request remote access to diagnose the problem. Once that access is granted, they can see every account, every saved password, and every financial document accessible from the computer.

In a related variant, the caller claims to be the bank’s fraud department, says accounts have been compromised, and instructs the victim to move funds to a safe account immediately. In a courier variant, someone arrives at the victim’s home to collect cash or gold the victim was told to withdraw. The FBI reported $2.13 billion in tech support and customer support fraud losses in 2025. The FTC found that adults 60 and older were significantly more likely than younger adults to report losses to these schemes.

The red flag

Any unsolicited request for remote access to your computer. Any instruction to withdraw cash, purchase gold or gift cards, or move funds to a new account to protect them.

The one rule

Legitimate technical support and financial institutions do not secure your money by asking for remote access, moving funds, or sending a courier for cash. Close the pop-up. Hang up. Call your provider using the number on your card or their official website.

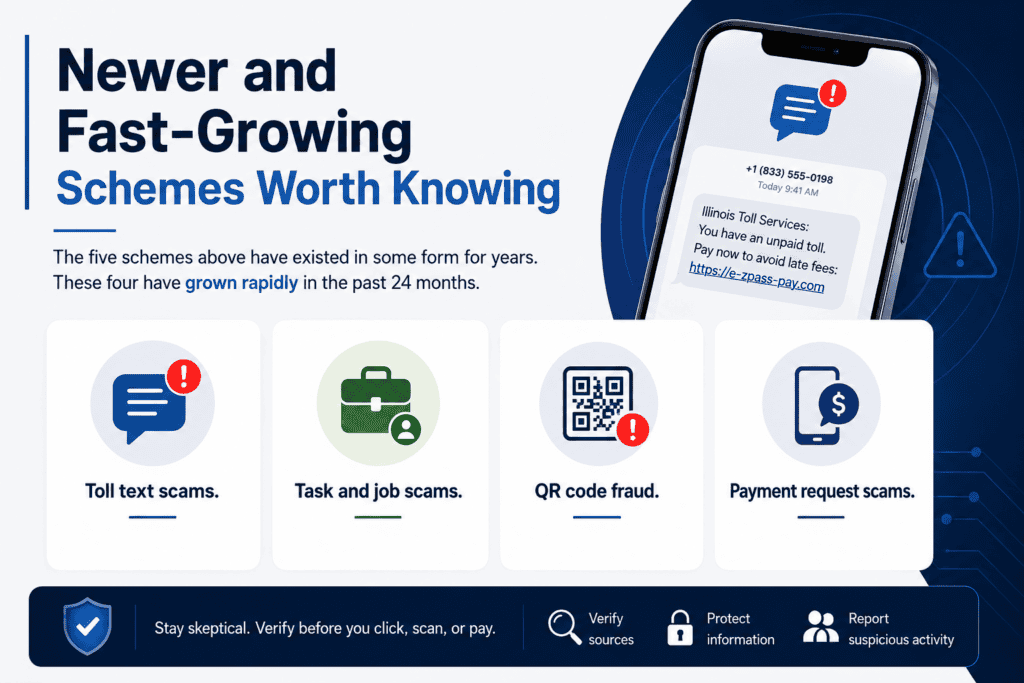

Newer and Fast-Growing Schemes Worth Knowing

The five schemes above have existed in some form for years. These four have grown rapidly in the past 24 months and are worth knowing because they may arrive in forms that do not look like the older schemes.

Toll text scams. A text arrives claiming an unpaid toll balance will result in a fine or license suspension unless paid immediately via a provided link. The FTC documented a 40 percent rise in government impersonation reports in 2025, driven significantly by these. They arrive constantly, affect all age groups, and the link leads to credential harvesting. The defense is the same: never use a link from an unexpected text.

Task and job scams. A text or direct message offers part-time remote work rating products or completing simple online tasks. The victim earns small amounts initially. Then a deposit is required to unlock the next level of earnings or to access a payout.

FTC data shows reports about task scams rose from roughly 5,000 in all of 2023 to approximately 20,000 in the first half of 2024. Real employers do not require workers to deposit money to receive pay.

QR code fraud. A QR code in a parking meter, restaurant, mailed notice, or posted flyer redirects to a fraudulent payment page or credential-harvesting site. The FBI reported a 99 percent increase in cryptocurrency ATM and QR code fraud complaints between 2023 and 2024. Before scanning any QR code in a public place, consider whether the source is one you would trust as a typed web address.

Cryptocurrency ATM fraud. A government impersonator or tech support caller directs the victim to a Bitcoin ATM to resolve a tax debt, legal matter, or account freeze. The FBI reported $247 million in cryptocurrency ATM and QR code losses in 2024, with older adults representing a disproportionate share of victims. No legitimate government agency, attorney, or financial institution directs payment through a cryptocurrency ATM.

On reporting: this matters

The FBI’s Operation Level Up found that 77 percent of victims were unaware a fraud was in progress at the time of contact. Many others who discover the fraud do not report it, often because of shame. That shame is misdirected.

These schemes were designed by professionals who study human psychology. Falling for one is evidence that the attack worked as designed, not evidence of poor judgment. Reporting matters for two reasons.

It opens a narrow window for fund recovery. And the FBI’s ability to identify patterns and notify other victims before they lose money depends entirely on the data it receives from people who come forward. If something here applies to your situation, report it first and process the rest later.

Time matters more than anything else in the first 24 hours.

Building the Defense

Knowing the schemes is the first step. The companion article, Your Fraud Defense Plan, covers what to build against each one: the family code word, the wire verification rule, the credit freeze, and the step-by-step response if something goes wrong. The Family Fraud Response Protocol is a one-page planning document designed to be kept with your estate documents and shared with family members.

If something in this article matched a situation you are currently aware of, that conversation should not wait. The window for fund recovery in most of these schemes closes within hours.

Have a situation that matches something here?

A complimentary conversation is available at no obligation.

We work through what happened, what may still be recoverable, and what structural defenses make sense going forward.

Schedule a Complimentary Conversation →

Langan Financial Group | 717-288-1880 | 1863 Center St., Camp Hill, PA 17011

Curious how today’s most sophisticated scams are specifically engineered to target your age group and your assets? Explore our fraud prevention resources to learn approaches that can help you recognize red flags before they become costly mistakes. Knowledge is one of the most effective tools available to protect what you’ve spent decades building.

This article is for educational and informational purposes only and does not constitute investment, tax, legal, or consumer protection advice. All investing involves risk, including potential loss of principal. Past performance does not guarantee future results.

Individual results will vary. The hypothetical scenario in this article is for illustrative purposes only, does not represent any actual client situation, and is based on documented patterns from FBI Operation Level Up case data. FTC 2025 fraud figures reflect the FTC Consumer Sentinel Network Data Book for calendar year 2025.

FBI IC3 2025 figures reflect the FBI Internet Crime Complaint Center 2025 Annual Report. FTC and FBI loss totals are not additive and reflect different complaint populations and classification methodologies. FBI IC3 investment fraud figure of $8.65 billion reflects FBI cyber-enabled fraud data for calendar year 2025.

FTC investment fraud figure of $7.9 billion reflects FTC Consumer Sentinel Network data for calendar year 2025. FBI Operation Level Up statistics reflect data through December 2025 (source: FBI.gov). FBI Recovery Asset Team 66 percent success rate reflects the FBI’s own reported figures; individual outcomes will vary and are not guaranteed.

FTC government impersonation growth of 40 percent reflects FTC 2025 Consumer Sentinel Network data. AI fraud complaint and loss data of $893 million across 22,364 complaints reflects FBI IC3 2025 Annual Report. AI-powered scam growth figure of 1,200 percent sourced from Vectra AI 2026 report on AI-powered scams.

Voice cloning indistinguishable threshold characterization based on published cybersecurity research cited in the Hiya State of the Call 2026 report. Hiya 1 in 4 deepfake call statistic sourced from the Hiya State of the Call 2026 report. FTC Consumer Protection Data Spotlight 2025 reference to voice sample harvesting from social media is an FTC-published finding.

QR code and cryptocurrency ATM fraud figures sourced from FBI IC3 2024 Annual Report. Task scam report growth figures sourced from FTC 2025 data. FTC text-based fraud losses of $470 million reflect FTC data for calendar year 2024.

All reported loss figures are minimums. investor.gov is a resource of the U.S. Securities and Exchange Commission.

FINRA BrokerCheck is a resource of the Financial Industry Regulatory Authority. Availability of these resources is not guaranteed by Langan Financial Group. Please consult qualified financial, legal, and consumer protection professionals before making any financial decisions.

Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.