Most parents do not want to stop helping. They want to help in a way that does not quietly cost them their retirement. This article shows you how to do exactly that, including the conversation most families have never had.

If you read our companion article on this topic, you may have recognized yourself in the numbers. Three out of four parents over 45 are financially supporting an adult child. A quarter of them have already postponed retirement as a result. And most of them have never sat down with their adult child to talk about what the support looks like, when it ends, or what it is doing to both sides of the ledger.

This article is not about cutting your child off. It is about helping on purpose, with a plan, in a way that works for both of you. That starts with a conversation most families treat as optional. It is not.

Why the Conversation Keeps Not Happening

Most parents know they should talk to their adult children about money. Most have not. According to Fidelity’s research, 38% of parents completely avoid the topic of retirement finances with their adult children.

The reasons are understandable. The conversation feels like a confrontation. It feels like a withdrawal of love. It risks anger, guilt, or a damaged relationship that took decades to build. So it gets postponed. And postponed again. And meanwhile, the money keeps flowing and the retirement plan keeps drifting.

Here is the reframe that makes the conversation possible: you are not having a money conversation. You are having a planning conversation. There is a difference. A money conversation is about what you are willing to give. A planning conversation is about what you are both building toward, and what role this support plays in getting there.

That reframe matters more than most parents realize. According to AARP’s November 2025 research of 1,744 adults 45 and older, 53% of the adult children receiving financial support are reportedly capable of meeting their basic needs with money left over. That does not mean the support is wrong. It means there may be more room to have this conversation than the situation feels like it allows. The need may be smaller than the habit.

And the conversation is already happening in most families, just not openly. More than three out of four supporting parents, 77%, now attach conditions to their financial help, up from 71% just a year earlier, according to Savings.com’s 2025 annual survey. Most parents are already trying to give with structure. They just have not said so out loud.

Most adult children do not know their parents are worried about retirement. Many parents find it difficult to talk about finances with their adult children, and their children may not have previously understood their retirement savings plan and how continued financial support may keep them from reaching those goals. When parents share that context, the conversation often goes better than expected. The child is not trying to drain a retirement account. They do not know one is at risk.

The Four Questions Worth Answering Before Any Conversation

Before you talk to your child, the more useful conversation is with yourself and your advisor. Four questions will tell you everything you need to know about whether your current approach is sustainable.

- 1.

What is the actual monthly total? Not the number you think of first. The real number: cash, rent, groceries, insurance, cell phone, loan co-signing, anything. Most parents underestimate this by 30 to 50 percent when they add it all up for the first time.

- 2.

Is this number in my retirement plan? Not vaguely accounted for. Explicitly included in a projection your advisor has run, with the support amount treated as a recurring expense. If it is not, your retirement projection is based on income that does not reflect your real spending.

- 3.

Is there a defined end point? Not a vague intention. A specific condition or date. “Until she finishes her nursing program” is a plan. “Until things get easier for him” is not.

- 4.

What does this support actually enable? Is it building toward something specific (a degree, a career transition, a business) or maintaining a lifestyle with no clear trajectory toward independence? There is no wrong answer, but knowing it clarifies what kind of conversation to have.

Answering these four questions gives you something concrete to bring to the table. Not a vague worry. Not an emotional ultimatum. A clear picture of what is happening, what it costs, and what you need it to look like going forward.

What the Most Common Types of Support Look Like and How to Restructure Each One

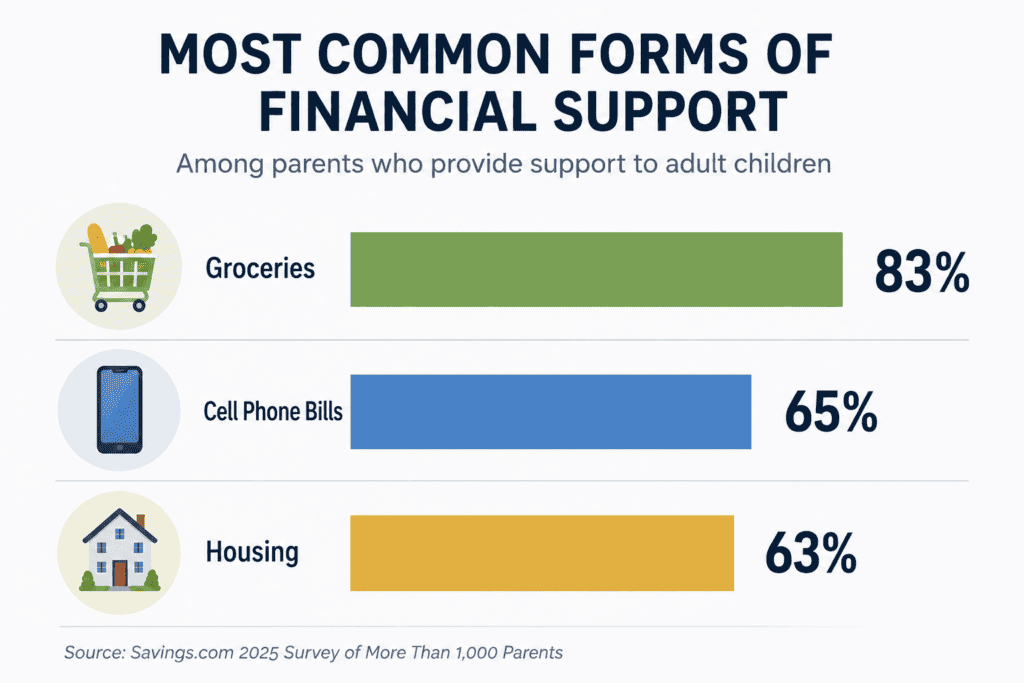

One of the most useful shifts a family can make is moving from unstructured monthly cash to a defined support structure. The amount does not have to change immediately. The shape of it does.

The most common categories, according to Savings.com’s 2025 survey of more than 1,000 parents: groceries (83% of supporting parents), cell phone bills (65%), and housing in some form (63%). Knowing which categories you are in helps you know which conversation to have first.

Groceries and everyday expenses: The Defined Bridge

Grocery support is the most common category and the most open-ended, because food is a recurring need with no natural finish line. The fix is to name a timeline or a trigger. “I will send you $200 a month through the end of the year while you are building your income. After that, I want this to be something you budget for.” That converts an indefinite transfer into a bridge. The support continues. The end point exists. Both of you know what it is.

Cell phone bills: The Simple Transition

Cell phone support often exists on autopilot. Many parents have been paying a family plan for years without ever explicitly deciding to keep doing so. This is one of the lowest-conflict transitions available: adding an adult child to their own plan typically costs $50 to $70 per month on their end, which is manageable for someone employed. A simple timeline works well here. “I want to move you to your own plan by [date]. Let me know if you need help setting it up.” The conversation is short. The transition is clean.

Housing and rent: The Milestone-Based Approach

Housing support carries the most emotional weight and the highest dollar amounts. The most effective approach is to connect it to a specific income milestone rather than an open timeline. “I’ll help with rent until you reach $X in monthly income, or until [date], whichever comes first.” That is not an ultimatum. It is a goal. The child knows what independence looks like in concrete terms. The parent knows when the support ends. One note: co-signing a lease creates a credit obligation and is worth discussing with an advisor before agreeing to it.

The Matched Contribution: building something, not just covering costs

Instead of supplementing spending, you contribute a dollar for every dollar your child saves toward a specific goal: an emergency fund, a down payment, or a retirement account. Research shows adult children who receive support with conditions attached are more likely to achieve financial independence than those who receive unconditional cash. The parent gives less over time. The child builds more. This works well when the child is employed but not yet financially stable.

Under the Affordable Care Act, adult children can remain on a parent’s health insurance plan until they turn 26. Many families have not thought about what happens after that. This is worth naming explicitly well before the birthday arrives. It gives the child time to plan, removes the surprise, and creates a natural transition milestone that does not require a difficult conversation. It is simply a date.

On the other side: if you are giving a lump-sum annual gift rather than monthly support, gifts up to $19,000 per person in 2026 do not require filing a gift tax return. Consult a qualified tax professional for guidance on your specific situation.

How to Actually Have the Conversation

The goal of the conversation is not to announce a decision. It is to reach one together. That distinction changes everything about how the conversation goes.

Start by sharing your situation, not delivering a verdict. Something like this:

“I want to talk about something I’ve been thinking about. I love helping you, and I want to keep doing that. But I also want to make sure we’re both clear on what this looks like going forward, because I’ve been realizing that I haven’t been as intentional about it as I should be. Can we talk through it together?”

This opening does three things. It names that the support continues. It removes the threat of an abrupt cutoff. And it frames the conversation as collaborative rather than corrective.

From there, share the specific thing you want to change. Not a general desire for them to “be more independent.” A specific proposal: a timeline, a milestone, a structure. Specific proposals are easier to respond to than vague appeals. They also make it possible to reach an agreement rather than just having a difficult conversation that changes nothing.

Avoid ultimatums framed as care. “I’m doing this for you” lands as dismissive, even when it is true. Focus on what you both need, not on what is best for them.

Avoid comparisons. What a sibling did, what you did at their age, what their peers are doing. These derail the conversation every time.

Avoid vagueness. “We need to figure something out” is not a plan. A date, a dollar amount, and a condition are a plan.

Give them time to respond and process. If this has been going on for a long time and was a well-established pattern, be prepared for the conversation to be difficult. Give your child a few days to process the news. Make it clear this is not a punishment. Most adult children, when given lead time and a clear picture, adapt. The ones who struggle most are those who had no warning and no transition plan.

Some children will push back. That is expected and does not mean the conversation failed. The goal of this first conversation is not to reach a final agreement. It is to start a dialogue that did not exist before. If your child reacts with frustration or silence, that is information, not a verdict. Give it time. Come back to it. A second conversation after a week of processing almost always goes better than the first one.

The Conversation You Also Need to Have With Your Advisor

The family conversation sets expectations. The advisor conversation sets reality. They are both necessary, and most families only have one of them.

What your advisor needs to know: the actual monthly amount, how long it has been going on, whether there is an end date, and whether it is currently in your retirement projection. If the answer to the last question is no, your plan needs to be updated before it can be trusted.

What the advisor conversation should produce: a clear answer to whether the current level of support is compatible with your retirement timeline. If it is, you can give with confidence rather than guilt. If it is not, you now know exactly what needs to change, which gives the family conversation a specific number to work with rather than a vague sense that something is wrong.

The goal is not to stop helping. It is to help in a way you have actually planned for, on a timeline you have both agreed to.

According to Ameriprise Financial’s 2025 research of more than 3,000 parents, 78% of those who worked with a financial advisor said their advisor helped them make better decisions specifically related to their adult children. The families who navigate this well are not the ones who gave less. They are the ones who gave with a plan.

What the Best Outcome Looks Like

A reader who has both conversations tends to arrive at the same place: they are still helping, but the help has a shape now. There is an amount. There is a reason. There is an end point, even if it is not imminent. And the retirement plan reflects it.

The child knows what to expect. The parent knows the support is not quietly working against the retirement they have spent decades building. Neither side has to carry the unspoken anxiety that comes from an arrangement nobody has ever formally acknowledged.

That clarity is the goal. Not less generosity. More intentional generosity, on terms that work for everyone.

If you have been giving without a clear plan, or if your retirement projection does not yet reflect what you are giving, that is worth a conversation. We can help you see the full picture and figure out what sustainable support actually looks like for your family.

Related reading: This article is the companion piece to Am I Putting My Retirement at Risk to Help My Children? which covers the research, the financial costs, and how to recognize whether support is sustainable. For guidance on the practical steps to reduce or end financial support, see our earlier article at langanfinancialgroup.com/how-to-stop-financially-supporting-your-adult-children/

Sources: AARP Research, “Parenting Longer,” November 2025 (survey of 1,744 adults 45+ with at least one adult child, conducted March-April 2025 by NORC at the University of Chicago; 53% capable of meeting basic needs figure). Savings.com, “Percentage of Parents Financially Supporting Adult Children Reaches a Three-Year High,” fourth annual survey, published March 2025 (survey of 1,001 U.S. parents of adult children, conducted February 2025; 77% conditions figure, 83% groceries, 65% cell phone, 63% housing). Fidelity Investments, research on parent-child financial communication (38% figure on avoiding retirement finance discussions with adult children). Ameriprise Financial / Artemis Strategy Group, “Parents and Finances,” 2025 (survey of 3,010 American parents, conducted January 2025; 78% advisor helpfulness figure). ACA health insurance age 26 provision: HealthCare.gov, Affordable Care Act Section 2714. Gift tax annual exclusion: IRS Rev. Proc. 2023-34; 2026 annual exclusion amount confirmed at $19,000 per recipient. Individual results will vary.

This article is for educational and informational purposes only. It does not constitute investment, tax, or legal advice. Gift tax rules are complex and depend on individual circumstances; consult a qualified tax professional before making gifting decisions. All hypothetical structures described are illustrative. Individual circumstances vary significantly. Consult a qualified financial and tax professional before making any decisions. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services offered through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.