Most retirees assume their financial plan covers how they draw income. Most of the time it covers how much, but not which account, and not in what order. These are different questions, and the gap between them is where a significant amount of unnecessary tax gets paid.

Three research reports published this week reinforce the same point: most people have not thought through how they will draw income in retirement. The TIAA Institute and Nuveen found that only 22% of workers have given serious thought to retirement withdrawals. BlackRock found that current savings rates are projected to replace only 50 to 60% of the income retirees expect their balances to generate. And the government’s latest inflation report confirmed prices are up 4.1% from a year ago, compounding the cost of every dollar drawn from the wrong account. The withdrawal question is not abstract. It has a dollar figure attached to it.

What to Look For

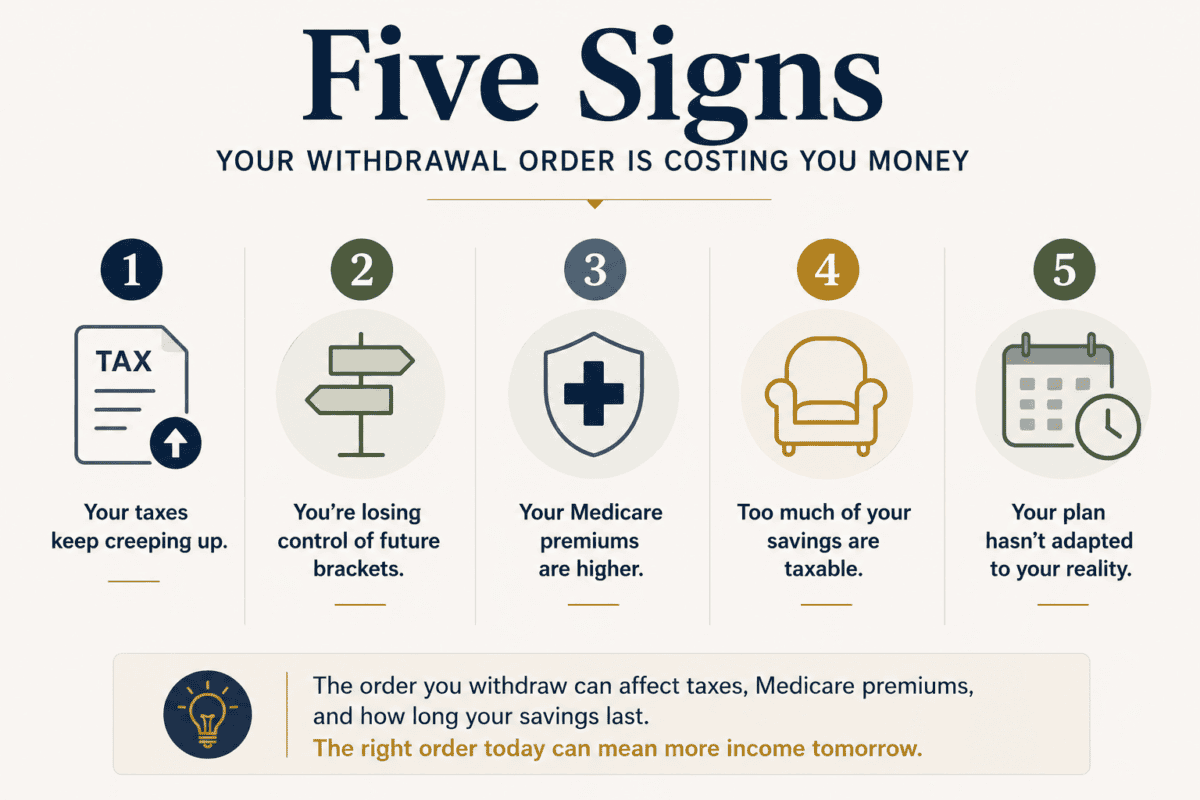

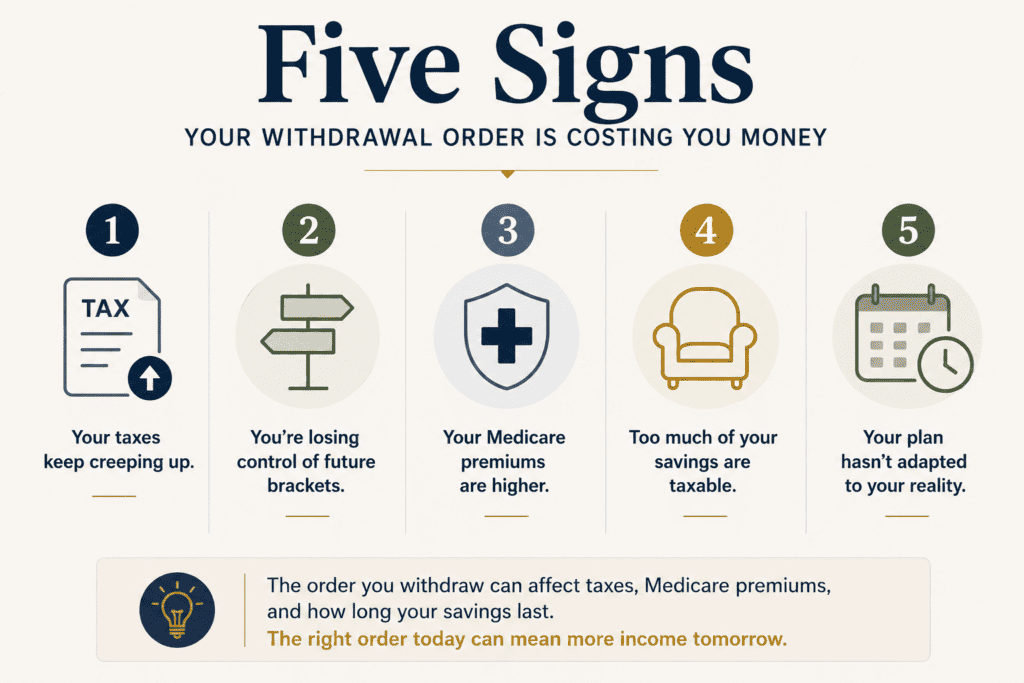

Sign 1: Your withdrawal is on autopilot

The most common pattern among retirees is to pick one account, usually a checking account linked to a brokerage or IRA, and draw from it automatically each month. The order was not chosen intentionally. It was set up for convenience and has been running on autopilot since. If you cannot explain why you draw from the accounts you draw from, in the order you draw from them, that is a meaningful gap. A withdrawal plan that was not consciously designed is probably not optimized.

Sign 2: Your IRA balance is growing in retirement

If your traditional IRA or 401(k) balance is higher today than it was when you retired, you are almost certainly drawing your income from other sources while the tax-deferred balance compounds. That may feel like a good thing. In many cases it creates a problem at age 73, when required minimum distributions begin and force withdrawals that can push income into higher brackets regardless of your actual spending needs. A growing tax-deferred balance in early retirement is not automatically a sign of good planning. It may be the early stage of a future tax spike.

Sign 3: You have not modeled your RMDs at 73

Required minimum distributions are calculated based on the account balance and the IRS life expectancy tables. If your traditional IRA or 401(k) reaches $700,000 or $800,000 by the time you turn 73, the required withdrawal in that first year is roughly $27,000 to $31,000, before considering investment growth. For a married couple with Social Security, that withdrawal alone may push combined income above $44,000 and trigger tax on up to 85% of Social Security benefits. Many retirees discover this at 73. The families who manage it well discover it at 62 or 65, when there is still time to adjust.

Sign 4: Your Roth has not been touched in years

Roth IRAs are not subject to required minimum distributions. There is no deadline forcing you to draw from them. That makes them easy to ignore and easy to let grow as a legacy asset. But there are specific situations in retirement where drawing from the Roth rather than the traditional account can significantly reduce your tax bill for that year. If your Roth IRA has not been touched in years and you are drawing exclusively from other accounts, it may be worth examining whether a different mix this year could keep your income below a key threshold. That threshold might be the point where Social Security becomes taxable, where Medicare premiums jump, or the edge of your current tax bracket.

Sign 5: Social Security, Medicare, and withdrawals are treated as separate decisions

The most common gap in retirement income planning is that these three income systems are treated as separate decisions. Social Security timing is one conversation. Medicare enrollment is another. Withdrawal amounts are a third. In practice, they interact in ways that can produce meaningfully different tax outcomes depending on the order and amount of withdrawals. If your financial plan does not show how withdrawal choices affect your Medicare premium two years from now, or how a large IRA withdrawal affects the taxable portion of Social Security, the plan has a gap that matters.

Five Questions to Answer Before Your Next Advisor Meeting

If any of the five warning signs above felt familiar, the following questions are worth answering before your next advisor meeting. You do not need to do anything with the answers right now. You need to know them.

- 1.

What is my current marginal tax bracket? Look at last year’s tax return. Find your taxable income on line 15 of Form 1040. For 2026, the 12% bracket for married couples filing jointly tops out at $99,600. The 22% bracket runs from $99,601 to $211,400. If you are in the 12% bracket, you have room to draw additional traditional IRA income this year without crossing into 22%. If you are already in 22%, you need to know how far from the 24% line you are before increasing withdrawals.

- 2.

What will my required withdrawals be at age 73, based on today’s balance? A rough estimate: divide your current traditional IRA or 401(k) balance by 26.5. That is the number the IRS uses at age 73 to calculate how much you must withdraw. The result is approximately your first year’s required withdrawal, before accounting for any growth between now and then. If that number, added to your Social Security income, puts you above your current bracket, the years before 73 are the planning window.

- 3.

How close is my income to the Social Security taxation threshold? For married couples, up to 85% of Social Security becomes taxable when combined income exceeds $44,000. Combined income means your other income sources plus half of your Social Security check. If you are near that threshold, the account you draw from can determine whether a meaningful portion of Social Security is taxed or not.

- 4.

Am I within two years of turning 65? Medicare Part B premiums are based on income from two years prior. If you are 63 or 64, income decisions this year and next determine your Medicare premium at 65 and 66. A large IRA withdrawal or Roth conversion in this window can raise your premium in the first two years of Medicare by several hundred dollars per month. The Medicare surcharge starts at $109,000 of income for individual filers and $218,000 for married couples in 2026.

- 5.

Has my advisor explicitly discussed withdrawal order with me? Not just how much to withdraw. Which account, and why, and how that interacts with Social Security and Medicare. If you cannot recall a conversation specifically about the sequencing of accounts, rather than just the withdrawal rate, that is the gap worth filling. According to Ameriprise Financial’s 2025 research, clients who have had explicit income coordination conversations with an advisor report significantly higher confidence in their retirement income plan than those who have not.

The right withdrawal order is not the same every year. It is an annual question, not a one-time setup.

What Comes Next

If the self-check surfaces a gap, the next step is not to immediately change your withdrawal approach. Withdrawal sequencing interacts with enough variables, including state taxes, estate goals, and specific account balances, that a change made without modeling the full picture can create a new problem while solving the original.

The right step is to bring the specific numbers to your advisor. Not a general question about whether sequencing matters. A specific set of inputs: your current tax bracket, your estimated required withdrawal at age 73, your total income relative to Social Security thresholds, and your Medicare premium situation if relevant. Those four numbers allow an advisor to model whether your current approach is optimal or whether an adjustment is worth considering.

Your current marginal tax bracket. From last year’s Form 1040, line 15 (taxable income).

Your traditional IRA or 401(k) balance today. Divide by 26.5 for a rough estimate of your required withdrawal at age 73.

Your combined income relative to $44,000 (married) or $34,000 (single) for Social Security taxation.

Your age. Specifically whether you are within two years of 65 or within ten years of 73. Both are key sequencing windows.

Whether your current plan explicitly addresses withdrawal order. If it does not, that is the starting point for the conversation.

The Annual Opportunity Most Families Miss

Rate environments shift. Tax brackets adjust. Required withdrawal amounts change each year. The interaction between your three buckets, Social Security income, and Medicare premiums creates an annual opportunity to manage your tax bill intentionally rather than defaulting into it. That does not change regardless of the rate environment.

Most families do not make bad withdrawal choices. They make unconsidered ones. The distinction matters because unconsidered choices can be reconsidered. The only requirement is that the question gets asked explicitly, with the numbers on the table.

If you have not had an explicit conversation about withdrawal sequencing, or if you recognized any of the five warning signs above, that is a useful conversation to have before the sequence has been running for another year.

Related reading: This article is the companion piece to Which Account Should You Draw From First? What the Research Says About Retirement Withdrawal Sequencing, which covers the research background, the three-bucket framework, and how sequencing interacts with the current rate environment.

Sources: TIAA Institute and Nuveen, 2025 Participant Sentiment Survey, published June 24, 2026 (n=2,100; 22% figure). BlackRock, 2026 Read on Retirement report, published June 25, 2026 (50-60% income replacement projection). Bureau of Economic Analysis, Personal Income and Outlays May 2026, published June 25, 2026 (PCE 4.1%). IRS 2026 tax brackets from IRS.gov. IRS Uniform Lifetime Table life expectancy factor at age 73: 26.5 (per IRS Publication 590-B, effective 2022). Social Security combined income thresholds from Social Security Administration. Medicare IRMAA thresholds for 2026 from Centers for Medicare and Medicaid Services. Individual results will vary.

This article is for educational and informational purposes only. It does not constitute investment, tax, or legal advice. Tax rules, brackets, and thresholds are subject to change. All withdrawal strategy examples are illustrative. Individual circumstances vary significantly. Consult a qualified financial and tax professional before making any withdrawal or tax planning decisions. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services offered through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.