Three out of four parents over 45 are financially supporting an adult child right now. Most of them have never calculated what that costs their retirement. This article helps you find out.

There is a question most parents in their 50s and 60s carry quietly. It rarely comes up with a financial advisor. It almost never comes up at the dinner table. But it is there.

Am I helping my children too much?

Not too much emotionally. Too much financially. Enough to put your own retirement at risk.

If you have felt that question but pushed it aside, you are not alone. According to a November 2025 AARP survey of adults 45 and older, three out of four are providing some form of financial support to at least one adult child. The average annual contribution is approximately $7,000. Many give far more.

This is not a lecture about stopping. It is an honest look at what the research shows and what the real costs are. More specifically, it will help you know whether what you are giving is manageable, or whether it is quietly working against the retirement you have spent decades building.

The Number Most Parents Have Never Added Up

Ask a parent how much they give their adult child each month and they will usually name the biggest item. The rent help. The car insurance. The occasional grocery run. What they rarely do is add it all together.

$1,474

Average monthly financial support parents give to adult children, a three-year high, according to Savings.com’s 2025 annual survey of more than 1,000 parents of adult children.

That is $17,688 per year. More than many people contribute to a 401(k). Working parents who support adult children contribute more than twice as much money to their children each month as they do to their own retirement accounts.

Read that again. More than twice as much.

This is not a judgment on those parents. Housing is expensive. Wages for younger workers have not kept pace with costs. Many adult children are genuinely struggling. The instinct to help is not only understandable, it is admirable.

But the instinct to help does not automatically account for what it costs. And that gap, between what parents feel called to do and what they have actually modeled in their retirement plan, is where the problem lives.

What It Means for Your Retirement in Real Numbers

Financial support to a child does not feel like a retirement decision. It feels like a family decision. But the money comes from the same pool.

Hypothetical Scenario: Individual results will vary

A couple at age 62 gives their adult child $800 per month to help with rent and groceries. That is $9,600 per year. Over ten years, at a conservative 6% average return, that same $800 monthly invested in a retirement portfolio could have grown to approximately $131,000. At age 72, when required minimum distributions begin, that gap grows further. Every dollar not saved also means less growth, more taxes on withdrawals, and less flexibility in how income is managed. The $800 monthly gift was a real retirement planning decision. It just was not treated as one.

According to the Savings.com research, 79% of parents who are financially supporting adult children worry about their own retirement savings. Compare that to 72% of parents who do not provide financial support. The gap is real, and the parents feeling it are not imagining things.

More striking: half of supporting parents say they would pull money from their savings or retirement accounts to help their children if needed. One in three say they would postpone retirement. These are not small concessions. These are permanent changes to the shape of a retirement.

~50%

Of parents supporting adult children say they have already sacrificed their own financial security to do so, according to Savings.com’s 2025 annual survey.

When Helping Your Children Delays the Day You Were Planning For

The worry most parents feel is real. So are the consequences.

According to a 2024 Bankrate survey of 2,377 U.S. adults with adult children, 43% of parents say financial support for their children has had a negative effect on their retirement savings. For 18%, the impact was significant. A separate survey by Intuit and Qualtrics found that 27% of parents who financially support adult children have postponed their own retirement as a direct result.

Pew Research Center’s 2024 study on young adult financial independence found the same pattern: 36% of parents who helped their children financially in the past year said doing so hurt their own financial situation at least somewhat.

These are not fringe outcomes. They are happening to more than one in four parents right now.

Hypothetical Scenario: Individual results will vary

David is 57. He has been giving his daughter $1,000 a month for three years to help with rent in a city where she is building her career. He plans to retire at 63. What he has not modeled is what those three years of support cost his retirement timeline. At a conservative 6% average return, $1,000 a month over three years could have grown to approximately $39,000 in his portfolio. If that pattern continues to age 63, the total foregone growth reaches approximately $86,000. His financial plan, last updated before the support started, still shows a retirement at 63. His actual plan, with the support factored in, may say 65. That is two years of retirement he did not know he was giving away.

The delay is not always visible. Retirement projections do not automatically update when money quietly leaves the household each month. The plan shows one picture. The reality is another. The gap between them only becomes clear when someone actually runs the numbers with the support included.

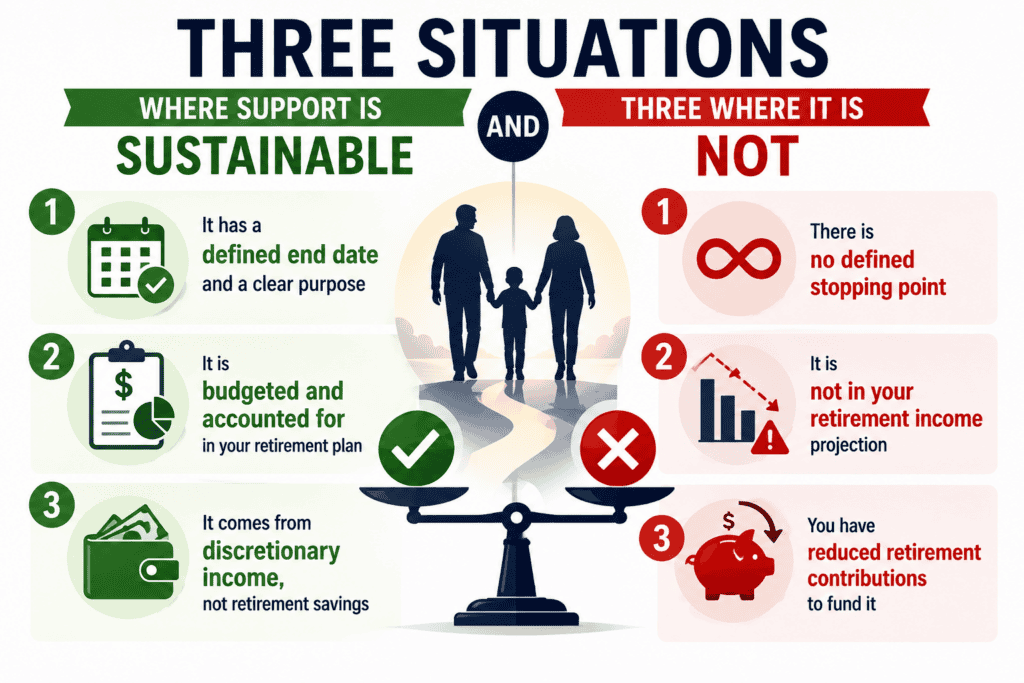

Three Situations Where Support Is Sustainable and Three Where It Is Not

The goal here is not a blanket answer. Every family is different. What matters is whether the support you are giving fits one of the sustainable patterns below, or one of the riskier ones.

Support tends to be financially sustainable when:

It has a defined end date and a clear purpose

Helping a child through a job transition, a medical event, or a specific financial setback with a plan and a timeline is structurally different from open-ended monthly support with no clear finish line. The first is a bridge. The second is a permanent income transfer.

It is budgeted and accounted for in your retirement plan

If your financial plan explicitly includes ongoing support to a child as a line item, and your retirement projections still work with that number in place, the gift is a choice. If it is not in the plan, it is a leak. Leaks are invisible until they are not.

It comes from discretionary income, not retirement savings

Giving from surplus spending money is very different from drawing on a retirement account or reducing contributions to fund a child’s expenses. The source of the money matters as much as the amount.

Support tends to create retirement risk when:

There is no defined stopping point

Open-ended support tends to extend. What begins as temporary help in a difficult year can quietly become an expected part of a child’s monthly budget and a permanent part of yours. According to the Savings.com research, fewer than 20% of supporting parents say their help will continue indefinitely, yet many have no specific plan or date to end it.

It is not in your retirement income projection

If your plan was built without including what you give your children, your projected retirement income is higher than your actual retirement income will be. That gap does not fix itself. The longer it goes unaddressed, the harder it is to close.

You have reduced retirement contributions to fund it

This is the highest-risk pattern. You cannot go back and contribute to prior years. Dollars not invested at 57 are permanently lost to growth. They will never have the time to build that dollars invested earlier would have had. The AARP research found that 9% of parents in their study had retired early specifically to provide more support to adult children.

Why It Is So Hard to Stop, or Even Slow Down

This is the part that most financial articles skip. The mechanics of the problem are not actually the hard part. The hard part is that you love your children, and stopping feels like withdrawing that love.

It is not. But it feels that way.

Research from the AARP’s November 2025 “Parenting Longer” study found that 92% of parents who provide financial support say they have a close relationship with the children they support. Only 8% say the support has hurt the relationship. Most parents giving money are giving it from a place of strength, not obligation or fear.

That makes it harder, not easier, to evaluate objectively. When something is coming from love, the calculation feels different. But the retirement math does not know the difference.

The permission most parents never receive

Setting limits on financial support is not abandoning your child. It is protecting your ability to be present, independent, and financially capable in the years ahead, including the years when they may need you in ways that money cannot fix.

A parent who runs out of money at 79 has not helped anyone, including the children they spent two decades supporting.

The Ameriprise 2025 research of more than 3,000 parents found that 65% believe they will have enough money for a comfortable retirement. But 36% worry that supporting adult children could affect those plans. That gap, between confidence and concern, is exactly where an honest conversation with an advisor tends to have the most impact.

“You can borrow money for almost anything in life. Retirement income is one of the few things you cannot replace once it is gone.”

The One Calculation Worth Doing Before Anything Else

Before any conversation about what to change, it helps to see the actual number. Not an estimate. The real monthly total of everything you give, across all forms: cash, rent, groceries, insurance payments, housing, and loan co-signing. Co-signing a loan counts too. It creates a financial obligation on your credit report and can affect your own ability to borrow if you ever need to.

Most parents who do this for the first time are surprised. A separate AARP survey of midlife adults found that more than half had given $1,000 or more to an adult child in the past year, and a quarter had given $5,000 or more.

Once you have the real number, two questions follow naturally:

First: is this number in my retirement plan? That means more than a mental note. It means your advisor has run a projection that includes this amount as a recurring expense, and the plan still works with it in place.

Second: does the plan still hold if this continues for another five years at this level?

If you cannot answer either question with confidence, that is the conversation worth having. Not with your child. With your advisor.

What Families Who Navigate This Well Have in Common

The Ameriprise research found something worth noting: 96% of parents who work with a financial advisor feel confident they can reach their top financial goals. And 78% said their advisor specifically helped them make decisions related to their adult children.

That does not mean the advisor told them to stop giving. It means someone looked at the full picture and helped them give in a way that was intentional, budgeted, and still compatible with the retirement they were building.

Families who handle this well tend to share a few things. They know the actual monthly number. They have discussed what the end of support looks like, even if it is not imminent. And they have modeled whether their retirement plan works with the support included, not assumed away.

None of that requires cutting off a child. It requires being honest about what you are doing and building a plan that accounts for it.

If you have been giving without knowing what it costs your retirement, that is worth a conversation. Not to stop helping, but to help with a plan behind it.

Sources: AARP Research, “Parenting Longer,” November 2025 (survey of 1,744 adults 45+ with at least one adult child, conducted March-April 2025 by NORC at the University of Chicago). AARP Research, “A Survey of Midlife Adults Providing Financial Support to Family Members” (separate survey; specific figures on $1,000+ annual support). Savings.com, “Percentage of Parents Financially Supporting Adult Children Reaches a Three-Year High,” fourth annual survey, published March 2025 (survey of 1,001 U.S. parents of adult children, conducted February 2025). Ameriprise Financial / Artemis Strategy Group, “Parents and Finances,” 2025 (survey of 3,010 American parents, conducted January 2025). Bankrate / YouGov, Financial Independence Survey, April 2024 (survey of 2,377 U.S. adults, 837 of whom are parents of adult children 18+). Pew Research Center, “Financial Help and Independence in Young Adulthood,” January 2024. Intuit / Qualtrics, survey on financial support and retirement postponement, 2023. All hypothetical scenarios are illustrative only, use simplified assumptions, and do not represent actual client outcomes. Individual results will vary significantly.

This article is for educational and informational purposes only. It does not constitute investment, tax, or legal advice. All examples are hypothetical. Individual circumstances vary significantly. Consult a qualified financial and tax professional before making any decisions. Securities offered through Cambridge Investment Research, Inc., a Broker-Dealer, Member FINRA/SIPC. Advisory services offered through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Langan Financial Group and Cambridge are not affiliated.